“Never let the future disturb you. You will meet it, if you have to, with the same weapons of reason which today arm you against the present.”

Marcus Aurelius Antoninus, Roman emperor from 161 to 180 AD, Stoic philosopher

WILL U.S. EXCEPTIONALISM CONTINUE TO POWER EQUITY MARKETS HIGHER IN 2025?

The iconic 1980s Back to the Future science fiction trilogy follows the adventures of small-town California teenager Marty McFly and his eccentric scientist friend Emmett ‘Doc’ Brown, as they travel through time in a modified DeLorean car, often finding themselves needing to alter the past to ensure their present future. The first movie was the highest-grossing release of 1985 and became an international phenomenon, leading to two sequel films, Back to the Future Part II (1989) and Back to the Future Part III (1990). In the second film, the characters travel into the ‘futuristic’ world of 2015, while they are accidentally sent back to the year 1885 in the third movie. Then-President Ronald Reagan even channeled ‘Doc’ Brown in his 1986 State of the Union Address, as he exhorted Americans to remember that “where we’re going, we don’t need roads.”

If the Back to the Future trilogy has a villain, it’s definitely Biff Tannen. In the second installment of the series, Biff, an egotistical, selfish, entitled and morally bankrupt bully, steals Doc’s DeLorean time machine, travels into the past, and gives his younger self a future copy of the Sports Almanac that contains the results of all sporting events from 1950 – 2000. Young Biff then uses the book to place one winning sports bet after another for immense financial gain. Eventually touted as the ‘luckiest man on Earth,’ he amasses a fortune and becomes one of the richest and most powerful men in America.

If we are honest, we have all wished at one time or another we could be in Biff's position - to possess an almanac of the future; to know what will happen tomorrow, next year, or next decade. Knowing the actual movement of markets would be a guaranteed road to riches, not unlike Biff’s fictional story. It sounds like an investor’s wildest dream, right? According to a recent study from Elm Partners Management’s Victor Haghani and James White, the surprising answer appears to be a resounding no!

The researchers placed participants in a dream position of knowing the future in an experiment called ‘The Crystal Ball Challenge.’ Players got an early read of major economic news and Fed policy decisions - without knowing the precise market moves of the day in advance - before placing their bets. They were given $1 million in play money and were shown 15 Wall Street Journal front pages following big economic news randomly selected over the past 15 years. With up to 50 times leverage, multiplying that pot of money sounds like shooting fish in a barrel.

Of the more than 8,000 mostly financially savvy players who had taken a crack at the game, Wall Street’s seasoned macro traders performed the best. Yet, when it came to predicting market directions, their score was far from stellar, with their median ending wealth after 15 rounds being just $687,986 - a loss of 31%! For amateurs, their returns took a hit as levered-up stock wagers went awry, with many losing everything.

The results will resonate with countless investors, where monetary and economic trends in the post-pandemic era have confounded even the smartest minds. “It’s very humbling,” said Haghani, who was a founding partner of Long-Term Capital Management. “Even if you have the news in advance, it’s still really hard to do asset allocation or whatever with a high chance of being right, let alone not knowing what’s going to happen.”

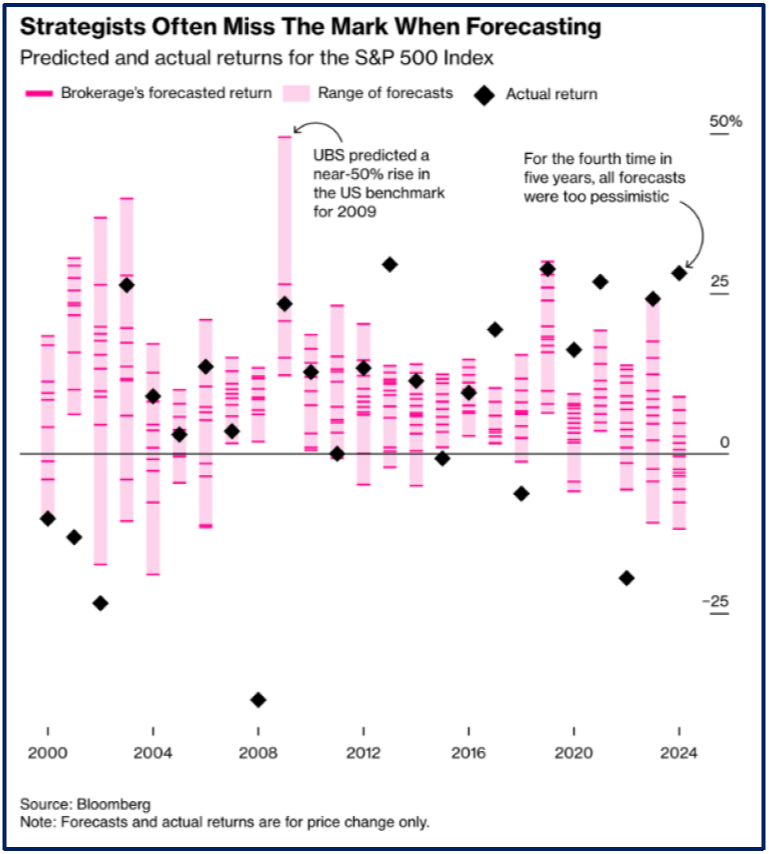

Why are we mentioning this? Because it’s a brand-new year, and that means champagne, Auld Lang Syne, weight loss resolutions, and Wall Street firms issuing their latest predictions for the S&P 500 in 2025. And they once again sound a lot like the predictions they made over the last few years. And the years before that. In fact, according to Bloomberg, over the past 25 years, 53% of the 376 brokerage return forecasts clustered between 0% and 10%. When comparing those past forecasts to actual year-end performance, they often appear less clairvoyant and more reflective of consensus expectations. In fact, analysts overestimated the S&P 500’s performance in 13 of the past 20 years, and they underrated its annual return in four of the past five years (see graph below).

After stellar back-to-back returns in 2023 and 2024, their average forecast for 2025 calls for the S&P 500 to deliver a gain of 9.1% - predictably within their preferred 0% to 10% range and in line with historical averages. With last year’s record-setting equity rally crushing even the most optimistic strategist forecasts, investors should view these year-ahead projections with a healthy dose of skepticism, understanding that they are inherently speculative and not information that actually matters to their investing strategy and situation.

A better, and ultimately more successful approach is to separate such irrelevant, distracting data (‘noise’) from relevant, meaningful, and valuable insights (‘signal’) for more accurate analysis and effective decision-making. Successful investors filter out the noise and stay focused on the long-term fundamentals.

2024: a year that exceeded expectations

It certainly paid off last year to ignore the ’noise‘ and focus on the ’signals‘. Investors entered 2024 generally with mixed emotions about the economy, fueled by worries about a potential recession, the Fed’s battle against inflation, the outcome of November’s national election, and the consequences of China’s downturn reverberating in global economies.

Yet as the year unfolded, it brought much for investors to like as the economy and markets defied many of those early-year predictions and challenged traditional economic models. Driven by robust consumer spending and strong earnings expansion, the ‘most anticipated recession ever’ never materialized this past year. Not only did the U.S. economy avoid a recession, it showed unexpectedly brisk growth, with real GDP expected to have expanded at a 2.7% pace in 2024.

On the strength of the growing economy, corporations continued to generate profit growth. For the full year, the basket of S&P 500 companies is expected to report year-over-year earnings growth of 9.4%, which can be attributed primarily to strong consumer spending.

After holding the federal funds rate at 5.25% - 5.50% from July 2023 to September 2024, the Fed initiated its first of three rate cuts with a jumbo 0.5% reduction in September, followed by two 0.25% cuts in November and December, signaling progress toward its dual goals of maximum employment and price stability. Inflation, as measured by the core PCE, the Fed’s preferred inflation gauge, showed a 2.8% year-over-year increase in November, indicating that inflation is cooling, albeit at a pace still above the Federal Reserve's long-term target of 2%.

It's interesting to note that while shorter-term bond yields declined significantly last year, yields on longer-term bonds trended higher as investors appeared focused less on the recent Fed rate cuts and more on continued solid economic data and inflation trends. Yields on the benchmark 10- year U.S. Treasury note, which traded at 3.69% on the day the central bank announced its first rate cut in September, jumped back up to end the year at 4.58%.

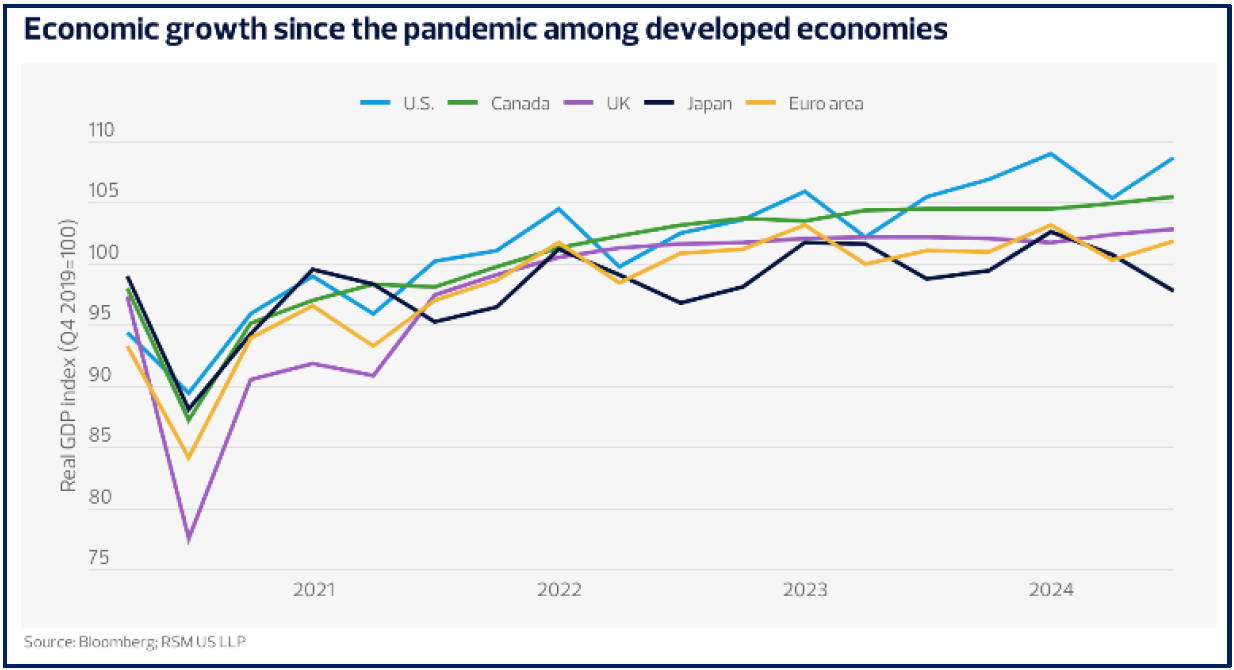

The resilient U.S. economy has particularly stood out when viewed in a global context by comparing it to other major economies. U.S. real GDP through the second quarter last year was 8.7% higher than at the end of 2019, as compared to Canada (5.5%), the UK (2.9%), or the EU (1.9%), which have experienced notably weaker recoveries. Germany’s real GDP is 2% lower and Japan’s 2.2% lower now than in 2019 (see graph above, courtesy RSM); while China’s economy is ensnared in a multiyear deleveraging process. As a result, U.S. equities have far outperformed those of other developed markets over the past decade, which has led to domestic stocks having much higher valuations than the equities in other developed markets.

In addition, U.S. stocks were widely seen as big beneficiaries of President-elect Donald Trump’s policy agenda. Capital markets reacted enthusiastically in the early days following the election victory as the market consensus believes the new administration is good news for American businesses and stocks. In particular, corporate and individual tax cuts, along with less regulation, should support business investment and consumer spending.

Amid post-election euphoria, U.S. small-business confidence surged to the highest level in nearly 3-1/2 years in November, according to the National Federation of Independent Business (NFIB). The small business sector is a crucial portion of the economy, generating more than 40% of U.S. economic growth and employment. Yet, while Trump will be supported by a friendly Republican Congress, translating campaign promises into policy is always difficult. As a result, policy uncertainty has replaced political uncertainty.

Driven by a strong U.S. economic backdrop, a healthy labor market, moderating inflation pressures, and robust corporate earnings growth, stock investors have enjoyed a powerful rally over the past two-plus years, with the S&P 500 index gaining 23.3% last year, building on a gain of 24.2% the prior year. It was just the fourth time in the past 100 years that the broad-based index logged 20%-plus returns two years in a row, according to research from Bank of America Securities. The Dow Jones Industrial Average ended up 12.9% on the year, while the equal-weighted version of the S&P 500 Index advanced 12.8% in 2024. And even though a ‘Santa Claus’ rally did not materialize in December, investors still had much to celebrate as investor enthusiasm around artificial intelligence (AI) supercharged a U.S. stock rally and boosted both Big Tech and smaller companies associated with the theme. That enthusiasm around the ‘Magnificent 7’ and other megacap stocks has contributed to historically elevated valuations, with the forward price-to-earnings (P/E) ratio on the S&P 500 at 22 times its projected earnings over the next 12 months, according to FactSet, above a 10- year average of 18.5 times and near a 20-year high.

Following the election, the ‘Trump trade’ reemerged, reviving what some have described as ‘animal spirits’ in markets, resulting in significant inflows into U.S. large-cap equity funds and cryptocurrencies that propelled key benchmarks, including the S&P 500, to new record highs and bitcoin to a 121% annual gain. ‘Animal spirits’ comes from the Latin ‘spiritus animalis’, which means ‘the breath that awakens the human mind’. The term was coined by famous British economist John Maynard Keynes to describe his view that investment prices tend to rise and fall based on human emotion rather than intrinsic value.

When the stock market is in rally mode, animal spirits play a significant role by driving investor optimism and confidence. Herd mentality ultimately amplifies market movements to a point at which stock prices rise far beyond their intrinsic value due to excessive optimism and speculation. The latest example of this is the proliferation of ‘Fartcoin’ (yes, you read that right), a meme cryptocoin with no utility or intrinsic value whatsoever. Not only does it exist, but its recent market value totaled $565 million, which is greater than 38% of all U.S. publicly traded companies! The warning sent by Fartcoin, according to Barron’s, may be silent but deadly.

Takeaways for 2025

Perhaps the most important lesson of 2024 is that markets can perform well in spite of investors’ worst fears. As we transition into 2025, the U.S. economy and stock market are entering the year from a position of strength, supported by strong underlying fundamentals. The pace of expansion will likely stay buoyant as the economy rides the tailwinds of both a fiscal impulse, courtesy of a market-friendly White House and Congress, and a monetary impulse from the Federal Reserve’s pivot to a rate-cutting cycle.

The Fed cut its benchmark interest rate by a full 1% last year, but central bank officials lately scaled back their projections for reductions in its federal funds rate this year. Policymakers are now penciling in only two rate cuts in 2025, fewer than previously forecast, with an end-of-year policy rate of 3.9%. They also made it clear that more reductions now hinge on further progress in lowering inflation.

Consumer spending, which accounts for nearly 70% of U.S. economic activity, should remain healthy, supported by rising real income and an extra boost from wealth effects, notwithstanding some stress among lower-income consumers who have been disproportionately squeezed by price inflation.

Given the expansionary fiscal policy that is expected - including tax cuts and increased spending, as well as less regulation - the U.S. economy is expected to grow between 2.2% and 2.5% in the year ahead amid full employment and price stability. U.S. companies should be well-positioned for continued profit expansion, with earnings for the companies that comprise the S&P 500 index estimated to increase by almost 15% this year, up from a projected 9.5% for 2024, according to FactSet.

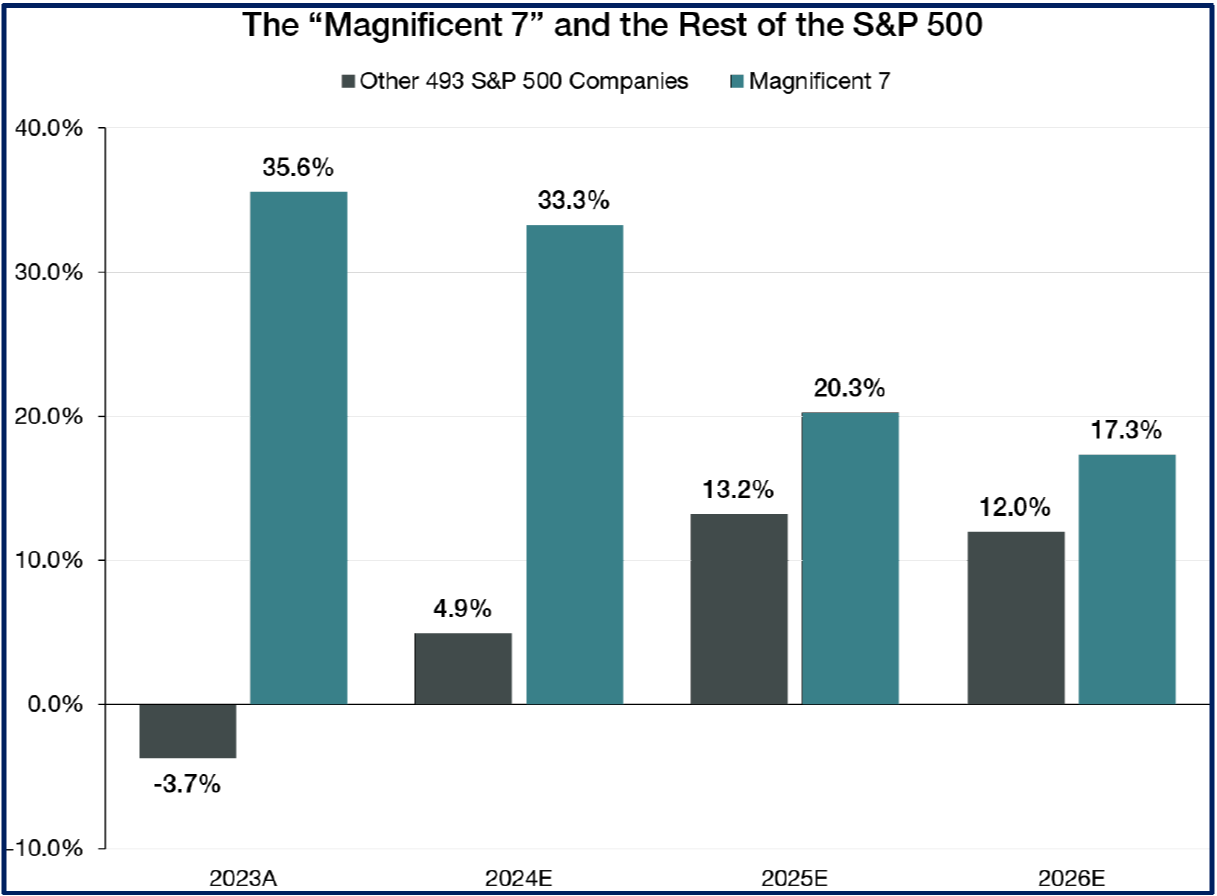

However, when we look at the composition of EPS (earnings per share) growth, there has been some noticeable movement: For a while now, a narrow segment of the market, primarily driven by the tech-heavy Magnificent 7, has had an outsized impact on U.S. stock performance. These mega-cap stocks now represent nearly 30% of the S&P 500. Their influence has led to the capitalization-weighted index’s higher returns and valuations. However, this dominance is starting to show signs of change. While analysts expect the Magnificent 7 companies to report earnings growth of over 20% in 2025, they expect the other 493 companies to report earnings growth of about 13% this year, which reflects a substantial improvement to expectations of just under 5% growth for these same companies for 2024 (see graph above).

The rapid evolution of AI will be a critical growth driver in 2025 as new models and applications make their way into mainstream use. U.S. exceptionalism is expected to bolster the U.S. dollar and buoy U.S. risky assets. At the same time, that macroeconomic backdrop, combined with America’s rising debt and deficits, suggests that long-term Treasury yields will likely remain ‘higher for longer’ as investors demand greater compensation for risk.

Still, much of the optimism about this year appears to be already priced into stocks, which leaves less upside room if conditions come in as expected and more downside risk if conditions come in worse than believed. Stock valuations across certain areas - especially certain U.S. large-cap stocks - are elevated, interest rates remain high and there is a risk growth could slow more than expected this year if Fed or fiscal policies turn from tailwinds to headwinds. Likewise, rising geopolitical risks in Ukraine and the Middle East, and increasing global economic tensions between the U.S. and China are also possible market impediments that could turn the tides. Such negative geopolitical and economic developments could expose the vulnerability of current stock market valuations and make for a bumpy ride.

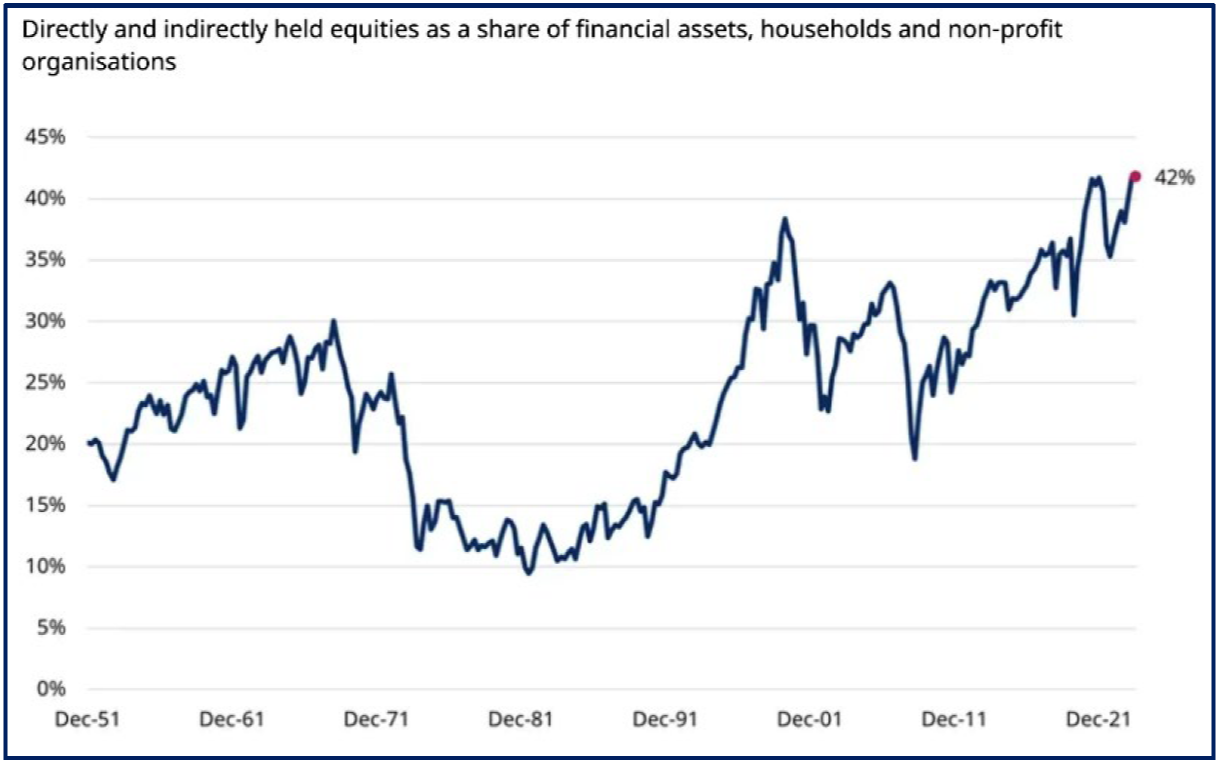

While today’s high valuations tell investors very little about what might happen over the next 12 months, crowded and overvalued markets have a greater risk of disappointment. Ultimately, high starting valuations will drag long-term returns down, which would suggest that market segments with the richest valuations today are likely to underperform over time. That’s particularly relevant now that the proportion of American consumers expecting stocks to move higher is at a 40-year high, and U.S. households never had so much of their assets invested in stocks (see graph below). Yet, as Schwab’s Liz Ann Sonders points out, ‘it’s hard to argue that high multiples in and of themselves represent a risk to the market’s near-term performance.’

So, while there’s currently no need for investors to worry about the S&P 500’s historically elevated valuations, now might be a good time for them to reassess their objectives and risk tolerances, and to consider how their various assets align with those goals. In particular, rebalancing portfolios to strategic asset allocation targets is critical for keeping a portfolio’s risk level in check. It may be prudent to lock in gains and reduce exposure to fully valued securities and allocate more capital to investments trading at more reasonable valuations to achieve one’s investment goals with less risk. We recommend that investors stay invested in the market, stick to a disciplined investing process, be diversified, and be prepared for a range of outcomes that could be broadly positive, but may also bring surprises and volatility that could affect their portfolios.

With an active approach to security selection, volatility management, and a time-tested investment process, our Telos wealth advisers are well positioned to navigate through changing economic and market conditions and can create a customized investment portfolio that incorporates your preferences and values to help you achieve your unique financial goals.

As we welcome a new year, our entire Telos family wishes you a bright and wonderful year ahead, filled with joy, health, abundance, and heartwarming moments with the people you love most! May your days be as balanced as your portfolio and your successes as compounding as interest. Happy New Year!

JANUARY 2025