“Be guided by beauty. Just as a great theorem can be very beautiful, a company that’s really working very well, very efficiently, that can be beautiful.”

Jim Simons, 1938 – 2024; hedge fund manager, mathematician, and philanthropist

WHY YOU WANT TO KEEP YOUR POLITICS SEPARATE FROM YOUR INVESTING

He had an appreciation for wit and was very interested in writing, but before he served in Vietnam, author Winston Groom didn’t have anything to write about. Going to war changed things. Raised in Mobile County, Alabama, Groom turned to writing in college. He graduated from the University of Alabama and then served four years in the US Army, including a tour of duty in Vietnam. After returning stateside, he moved to New York City and completed his first novel, ‘Better Times Than These’, set in the Vietnam War and published in 1978.

While on a trip home to Mobile, his father told him a story about a neighbor’s child who despite mental challenges displayed savant behavior. Inspired, Groom started to take notes and by late that evening he had written the first chapter of ‘Forrest Gump’. He finished the book in just six weeks, but the novel made little impact upon its release in 1986 and all but faded into obscurity.

Then came July 6, 1994, when the film version of ‘Forrest Gump’ - directed by Robert Zemeckis and starring Tom Hanks, Gary Sinise, and Robin Wright, among others - was released nationwide to widespread critical acclaim. The epic comedy-drama chronicles the charmed life of a mentally challenged man and the accidental role he plays in some of the 20th century’s most memorable events, such as teaching dance moves to a young Elvis, meeting President John F. Kennedy with the University of Alabama football team, and being interviewed on The Dick Cavett Show next to John Lennon. It was a huge success, both culturally and commercially, earning nearly $700 million at the box office and winning six Academy Awards, including Best Picture, Best Director, and Best Actor.

On the 30th anniversary of its release, the inspirational movie remains a classic, maintaining its winning, heartening, and indelible place in American culture. In fact, some of its memorable quotes have become so ingrained in our culture that even if you haven’t seen the movie, you probably know what the famous line “My mama always said, ‘Life is like a box of chocolates – you never know what you’re gonna get’” means.

This iconic quote has permeated popular culture since the film’s release in 1994. It’s a gentle reminder that varying degrees of risk and uncertainty are always present, whether in the field of investments or simply in our daily lives. That is particularly true this year, with 2024 being a historical election year. Nearly half the world’s population will vote in major elections this year, casting ballots in at least 70 countries that represent over 60% of the world’s economic output (GDP). The outcome of those elections will shape public policy in every corner of the globe and could usher in major shifts in domestic and foreign policy.

Elections have consequences for financial markets. From Mexico to India to South Africa, surprising election results have already rocked markets recently. In France, the threat of electoral losses for the president’s centrist party sent the French stock and bond markets to their worst week in more than two years. Approaching soon is July’s election in the United Kingdom. And later this year, the U.S. presidential election in November might unleash its own volatility on markets. It all adds up to a lot of uncertainty for financial markets that notoriously hate it.

Concerns over the November U.S. elections jumped to the second greatest threat in the Fed’s Spring 2024 Financial Stability Report, with 60% of those surveyed citing this as a risk, up from just 24% in October last year. A separate KPMG survey revealed similar concerns, with 62% of CEOs saying they would delay investment until after the election.

Domestic stocks have shrugged off the uncertainty so far and posted their best first-half performance during an election year since 1976 as the market has yet to fully engage with the election narrative. Investors appear to be more focused on whether and when the Fed will begin lowering interest rates, with the expectation that such a move could further improve the investment environment. However, as the November vote approaches, investors are likely to be more attuned to the potential ramifications since presidential elections always add an extra element of uncertainty to financial markets and the economy. In fact, during election years, and especially as the election approaches, market volatility tends to be higher, and returns tend to be lower because markets generally do not like uncertainty.

To be sure, the political order can have sweeping impacts on policy and society. However, election outcomes are not as transformative as macroeconomic factors, such as monetary and fiscal policy, inflation, labor markets, consumer spending, or corporate profits, which exert substantially greater influence on the economy and markets. Accordingly, electoral outcomes are not material drivers of the economy or markets, and both have historically fared well under nearly every partisan combination.

How should investors approach investing in an election year?

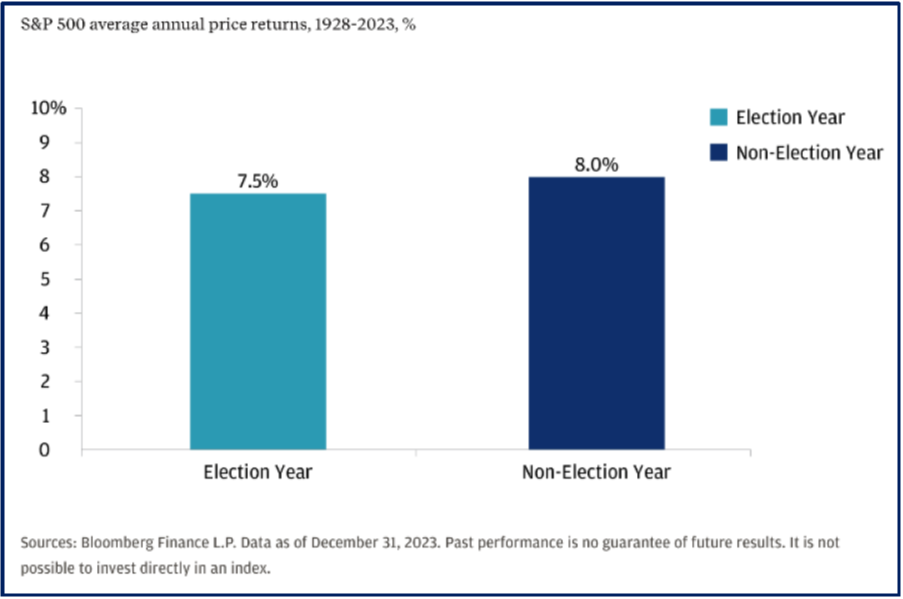

Stock returns in election years

Since 1928*, the average annual returns for the S&P 500 Index were modestly lower in U.S. presidential election years (7.5%, on average) compared with non-election years (8%, on average), according to J.P. Morgan (see chart above). While the benchmark typically rose during election years (positive in 18 of the past 24), there was substantial variation in returns between the S&P 500’s best election year (+37.1% in 1928) and its worst (-38.5% in 2008). The good news for investors is that the S&P 500 has already far surpassed those average gains, surging 14.5% so far this year.

*The market performance data used goes all the way back to 1928. However, only 24 presidential elections have occurred over this period, so it’s difficult to draw statistically significant conclusions about how those elections impacted stock market returns.

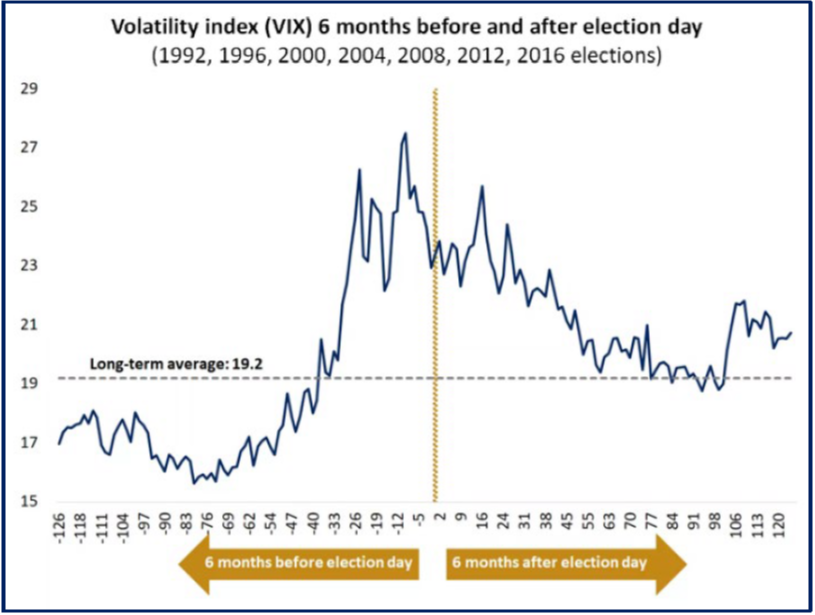

Volatility is likely to rise

While volatility is a feature of investing in any year, election years tend to be more volatile, especially just before the vote as anxiety and uncertainty tend to rise in the lead-up to the first Tuesday in November. This may explain why market volatility (as proxied by the CBOE Volatility Index, or VIX) has tended to rise notably two months before election day (see chart above, courtesy Edward Jones). By 30 days after the vote, however, volatility historically subsided somewhat and returned to normal 60 days post-election.

Markets are nonpartisan

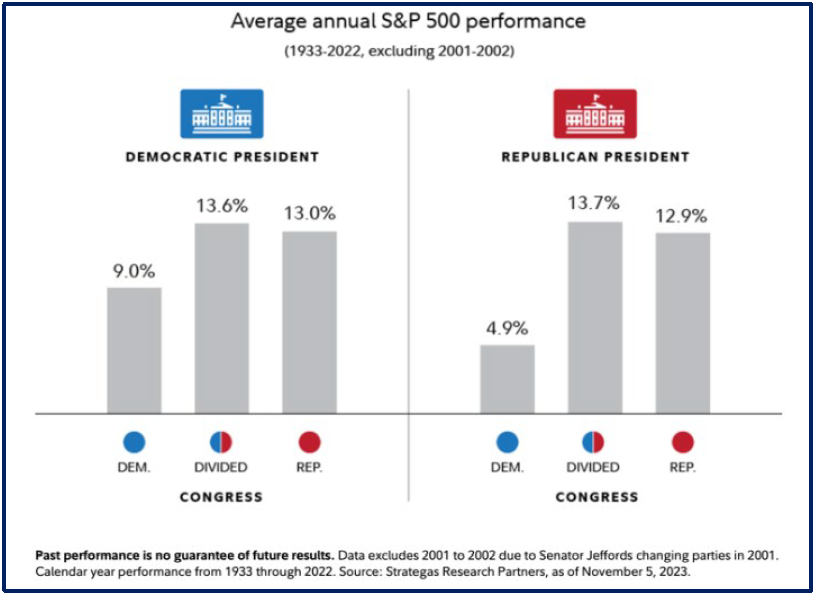

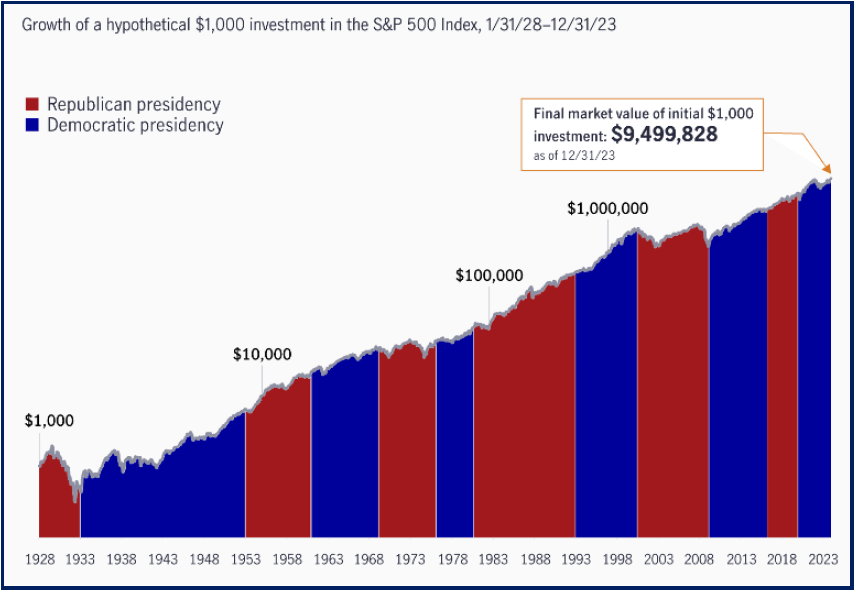

Investors often wonder whether the market will rise or fall based on who is elected president. Looking at the historical data, it appears that capturing the long-term returns in the capital markets does not depend on which party controls the White House. As the chart below shows (courtesy of Fidelity), the S&P 500 has historically averaged positive returns under nearly every partisan combination. In fact, there’s evidence that a divided government historically coincided with stronger market returns - perhaps because government gridlock creates less disruption and fiscal policy uncertainty.

Remember, that regardless of whether the federal government is red or blue, the factors that affect stock prices - whether positive or negative - are in most cases not influenced by the government, but by interest rates, the economy, and geopolitical conditions.

Fundamentals drive market performance

The health of the economy seems to play a critical role in whether the incumbent party remains in the White House or the challenger wins the presidency. As famously quoted by James Carville, campaign strategist for Bill Clinton, ‘It’s the economy, stupid.’ He was right. The economic landscape during a sitting President’s term frequently shapes their perceived success.

According to research by T. Rowe Price, in more than 70% of election losses for the incumbent party, the economy had been in a recession that year or slipped into one during the following 12 months. Hence, the soft-landing scenario envisioned by the majority of economists will likely have an impact on the presidential election as voters tend to vote with their wallets.

As we mentioned earlier, data shows that market returns are typically more dependent on economic and inflation trends, rather than election results. In general, rising economic growth and falling inflation have been associated with returns that are considered above long-term averages. For investors, staying focused on economic fundamentals, such as the stage of thebusiness cycle, corporate profits, productivity, the level and direction of interest rates, as well as the job market, is undeniably more insightful than potential election outcomes. Additionally, powerful secular trends like advancements in artificial intelligence (AI) are poised to maintain momentum, irrespective of who occupies the White House. So, rather than trying to predict near-term political or market cycles, investors would be better served by adopting a thoughtful long-term financial plan that’s suited to their needs, and sticking with it.

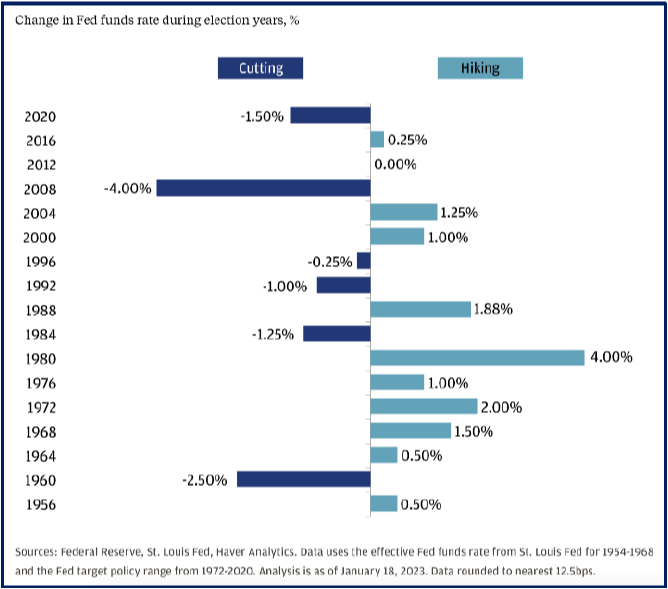

Will the Fed cut rates before the election?

Election years often bring concerns that the Fed would refrain from making significant policy moves. After all, the Fed is supposed to be politically independent and a rate hike or cut could carry implications of a political motive. History shows that the Fed has not shied away from hiking or cutting rates during election years. In fact, since 1956, the central bank has raised or lowered interest rates in every election year save one - 2012 (see chart below, courtesy JPM).

During its June meeting, the Federal Open Market Committee (FOMC) kept the federal funds target rate steady at 5.25% to 5.50% and reduced its outlook for interest rate cuts in 2024 to just one, down from its March projection of three reductions, as it continues to pursue its dual mandate of price stability and maximum employment irrespective of elections. Besides, interest rate cuts this close to the election are unlikely to change economic factors that affect voter attitudes, such as unemployment, persistent inflation, or resilient growth.

Policy issues with economic impact

While elections generally don’t produce a meaningful medium- to long-term influence on the economy or the broader markets, actual policy shifts are likely to create relative winners and losers at the asset class and sector levels. Sectors, such as health care, traditional energy, clean energy, aerospace and defense, tend to be more sensitive to the likelihood of a particular candidate winning the election. Furthermore, control of the U.S. Senate could be key to bringing about significant changes in policy regarding taxes, spending, and regulation.

Here are some of the policy issues to monitor throughout the presidential election process:

- Individual and corporate tax policies

- Spending priorities, such as infrastructure, defense, energy

- Business regulation

- China (trade and Taiwan)

- Immigration

- Geopolitical conflicts (Ukraine, Middle East)

Given today’s polarized political environment, we believe proposed policies are worth monitoring for their potential impact on specific industries, company fundamentals, as well as the broader economy.

Tax implications

The winner of November’s presidential election will face an epic challenge next year with the coming expiration of nearly $4 trillion in tax cuts at the end of 2025. Enacted by former President Donald Trump, the Tax Cuts and Jobs Act of 2017 (TCJA) included lower federal income tax brackets, bigger standard deductions, and higher gift and estate tax exemptions, among other provisions. This means lawmakers will have to decide on how to tackle changes to the tax code, striking a balance between raising taxes and further increasing national debt. Expiration of the TCJA law would lead to fewer deductions and increased taxes for more than 60% of U.S. tax filers, according to the Tax Foundation.

With control of Congress and the White House uncertain, it’s difficult to predict which TCJA provisions, if any, could be extended. However, smart planning now could provide significant savings for investors and their heirs down the road. Steps to minimize the potential impact could include Roth IRA conversions, reducing your taxable estate, and making large charitable contributions. To effectively navigate the complexities of the TCJA sunset and achieve your tax- and estate planning objectives, contact your Telos wealth adviser or your estate planning attorney to discuss your specific circumstances and how to best attain your desired estate planning goals.

Key Takeaways

It’s been said that life is 10% what happens to us and 90% how we choose to react to it. Election season can stir up strong emotions in investors that cause them to become increasingly concerned about the ramifications of an election on their portfolios. Not to mention that most of the election-related advice coming from news sources is geared toward triggering an emotional reaction in them, that’s both conscious and subconscious, and not necessarily in their best interest from a long-term perspective. In the media, this fact is so well known that you’ve probably heard the industry adage, ‘if it bleeds, it leads.’ Suffice it to say that good news doesn’t grab your attention, but dire predictions probably will.

The urge to re-allocate toward risk-off strategies when political noise is at its peak is understandable but runs contrary to U.S. equities’ historically strong election year performance record. As the accompanying chart on this page shows, stocks have traditionally performed well, irrespective of which political party holds the presidency. Arguably, economic variables, such as earnings, profit margins, the business cycle, interest rates, and innovations, have been and will likely remain the market’s most important drivers; not election outcomes.

The economy is typically a chief concern for voters, and their assessment of economic conditions, along with the candidates’ ability to manage it, will likely have a strong impact on the outcome of the race. A year ago, economists saw a recession as very likely and projected anemic growth for the year ahead. Instead, the U.S. economy grew by a bustling 3.1% in 2023, shaking off recession fears and offering an upbeat picture of consumers and businesses. The pace of the expansion slowed sharply in the January – March quarter this year to a 1.4% annual pace as a consequence of the Fed’s commitment to a higher-for-longer approach to interest rates due to persistently sticky inflation. While the consensus forecast for the economy remains cautiously optimistic, with most analysts projecting either a soft landing or no landing at all, the uncertainty and noise triggered by the election will likely exacerbate that downtrend.

Equity markets have demonstrated remarkable resilience so far this year, with both the Nasdaq Composite and S&P 500 trading at all-time highs, even as macroeconomic concerns weighed. Strong corporate earnings - expected to grow 11% this year and 14% in 2025, according to FactSet -, a still resilient consumer, and eagerness to own a piece of an AI-charged future provided a supportive backdrop for stocks and propelled the S&P 500 to a staggering 31 record closes since January. Despite a series of hot inflation readings that damped investors’ hopes that the Fed would soon begin to cut interest rates, the S&P 500 Index soared 14.5% in the first half of this year, with a handful of ‘Big Tech’ stocks accounting for well over half of the broad U.S. stock index’s return so far this year, even as the majority of stocks substantially trailed the leading tech-related sectors. By comparison, the S&P 500 equal-weighted index is up just 4% in the first six months, underperforming the capitalization-weighted index by over 10% and extending the widest gap in a calendar year going back to 1990. The concentrated rally in an ever-narrowing cohort of tech stocks also left the blue-chip Dow Jones Industrial Average behind, which advanced merely 3.8% so far this year.

Bond yields ended the first half with two consecutive quarterly increases, with the yield on the benchmark 10-year U.S. Treasury note climbing to 4.34% from 3.86% at the end of last year. Tellingly, neither Biden nor Trump appears willing to arrest out-of-control spending, so under either administration, spiraling U.S. debt may cause investors to demand a higher premium to own longer-dated Treasuries.

The U.S. election cycle will heat up as November approaches, with the potential for bouts of market volatility to ensue, particularly since elevated valuations could make stocks susceptible to disappointments of any kind. Yet as we highlighted, the historical data and empirical evidence shows that maintaining allocations in diversified portfolios that can weather short periods of elevated market volatility, and not basing investment decisions on political parties, is the most probable way to increase total returns. We believe that our tried-and-true strategy of patience and discipline in the face of uncertainty is the best way to keep portfolios on track to achieve your financial goals and benefit from continued long-term market appreciation and economic growth. The old adage, ‘time in the market beats trying to time the market,’ has been proven true over the years. Or in the words of Warren Buffett, arguably one of the world’s greatest investors: ‘We don’t have to be smarter than the rest. We have to be more disciplined than the rest.’ Because in life, as in investing, ‘you never know what you’re gonna get!’

JULY 2024