“With a good perspective on history, we can have a better understanding of the past and present, and thus a clear vision of the future.”

Carlos Slim Helu, 1940 - present; Mexican business magnate, investor and philanthropist

RIDING THE TAILWINDS: OUR INVESTMENT OUTLOOK FOR 2026

Gatlinburg, a mountain town in eastern Tennessee, is the kind of place where memories are made. Known as a gateway to the roughly 520,000-acre Great Smoky Mountains National Park, the small town draws millions of visitors each year with its cozy Appalachian charm and abundant year-round outdoor activities.

Come December, the town transforms into a dazzling winter wonderland, with the Fantasy of Lights Christmas Parade as its crown jewel. The parade is a full-blown spectacle of twinkling lights, festive music and a grand appearance by Santa Claus that turns downtown Gatlinburg into a glowing holiday wonderland. The town’s 50th annual parade, held last month, was no exception, bringing together more than 80,000 locals and visitors for a joyous holiday celebration.

Yet perhaps the most talked-about moment of the evening was a total surprise. A seemingly unfazed black bear made an unexpected appearance, calmly strolling down the parade route and becoming the star of the show in front of a crowd of onlookers, creating a viral moment that both stunned and delighted spectators. The incident highlighted the prevalence of bears in the Great Smoky Mountains National Park - home to an estimated 1,500 black bears - even as spectators enjoyed the unexpected, furry guest.

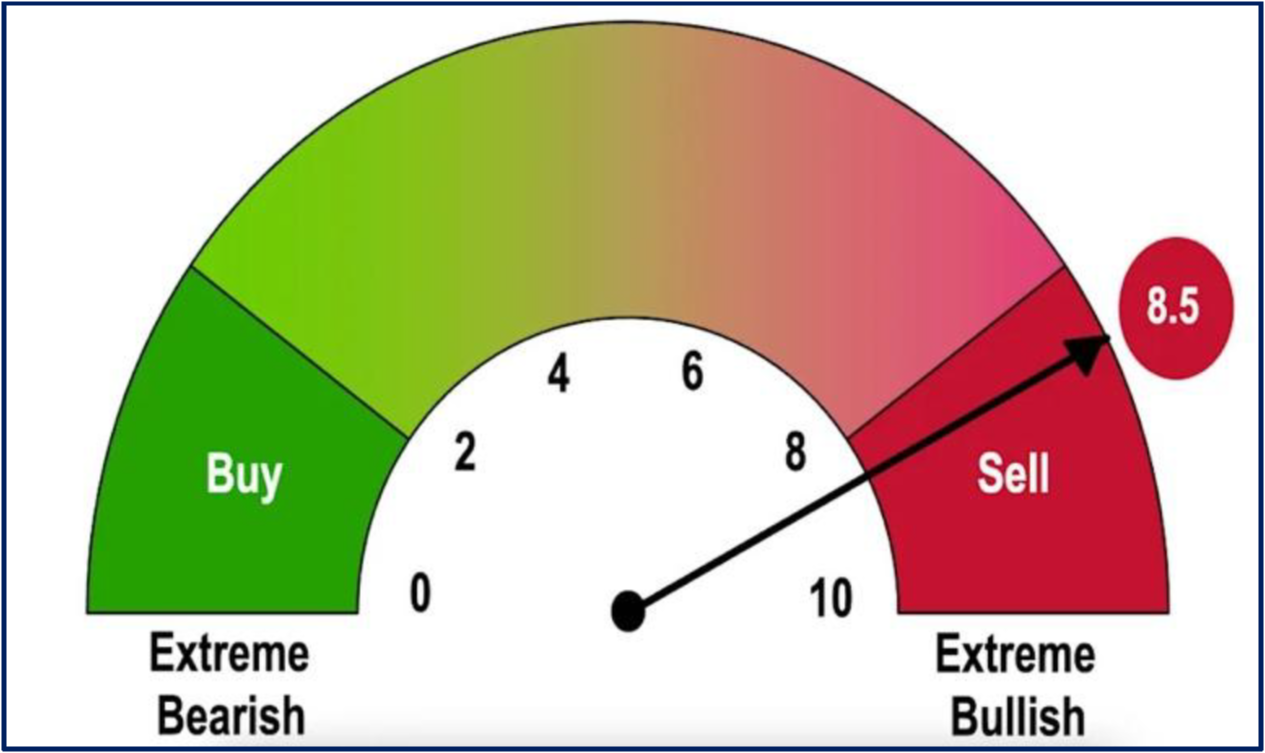

In contrast, bears seem to be hibernating on Wall Street, if not extinct altogether, as bullish sentiment has continued to drive equity markets higher. The relentless gush of cash into the stock market, however, is sending a powerful ‘sell signal’, according to a Bank of America Merrill Lynch gauge that has a formidable track record. Their proprietary Bull & Bear Indicator*, which is derived from BofA’s regular fund manager survey, which asks 200-plus investment managers about their appetite for risk, has moved into extreme bullish territory, rising to 8.5 from 7.9 and triggering a contrarian sell signal for risk assets as fund managers may be getting too bullish for their own good (see graph below). The premise behind the Bull & Bear Indicator is straightforward: when everyone is on the same side of the boat, even a small shift can tip the balance, leaving markets vulnerable to sudden corrections. Indeed, readings above 8.0 have often preceded pullbacks, with global equities declining a median 2.7% over the following two months, with a 63% historical accuracy rate.

*[Wall Street uses the bull and bear analogy as shorthand for the stock market's general mood and direction. A bull market is a period of rising prices and investor optimism, while a bear market is characterized by falling prices and widespread pessimism].

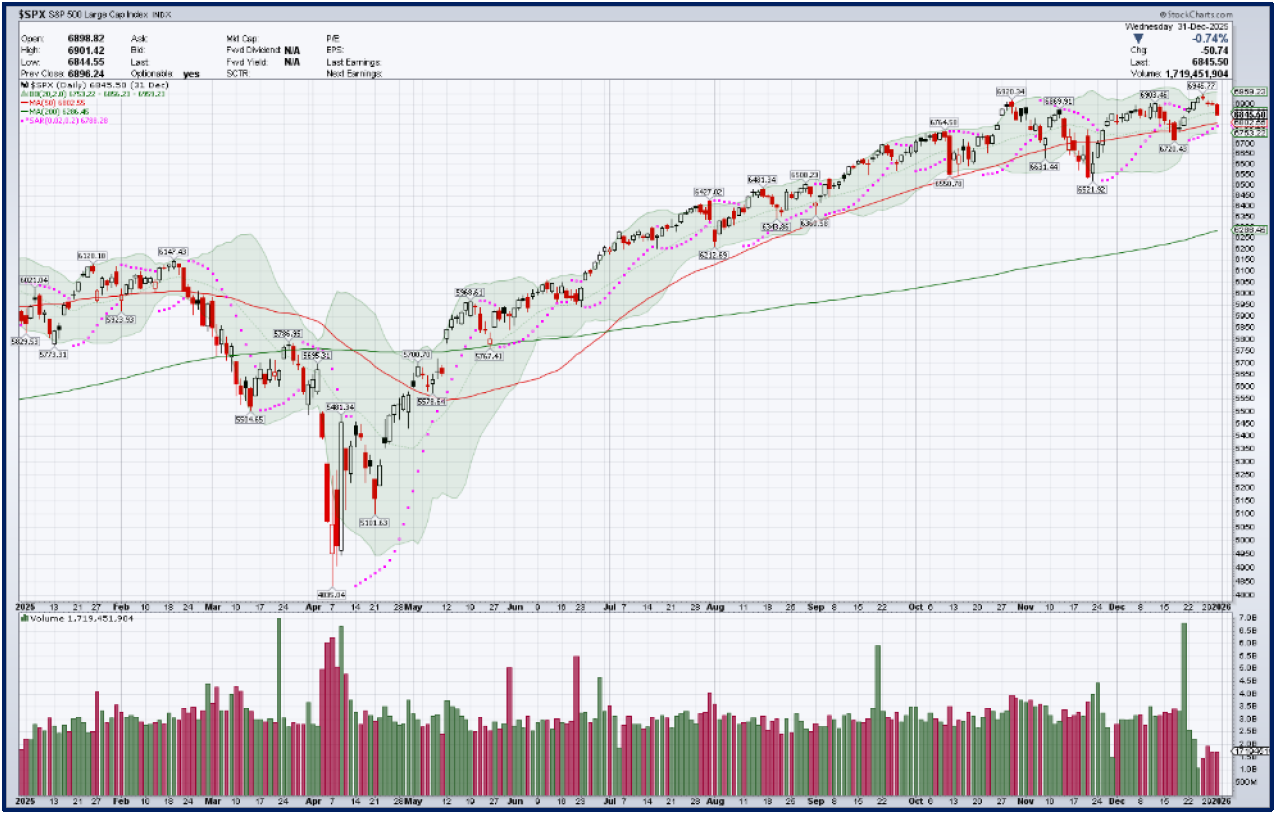

This surge in bullish sentiment is particularly notable given the level of turbulence market participants faced over the past year. After two years of relative calm, market volatility returned in 2025 as President Trump announced and enacted numerous tariffs, sending the S&P 500 nearly 20% below its peak in just seven weeks and stopping just short of bear market territory (defined as a 20% decline or worse). However, the market staged a stunning comeback after the administration announced a 90-day pause on reciprocal tariffs for ‘non-retaliating’ countries in April, as investors refocused on generally strong fundamentals, including healthy consumer spending and solid corporate earnings growth. Easing trade tensions, steady economic momentum, and ongoing enthusiasm around AI further supported market gains. For the year, the S&P 500 gained 16.5%, notching its third consecutive year of returns exceeding 15%. That same AI boom contributed to a 20.4% annual gain in the Nasdaq Composite, the best-performing U.S. equity index.

AI adoption also continued to serve as a powerful long-term driver of economic expansion and corporate profitability, supporting earnings growth across key sectors, with technology and communication services among the S&P 500’s top-performing sectors for a third consecutive year, each gaining more than 24%. These sectors also posted the strongest earnings gains, with profits projected to climb over 17%, once again underpinned by robust AI investment trends.

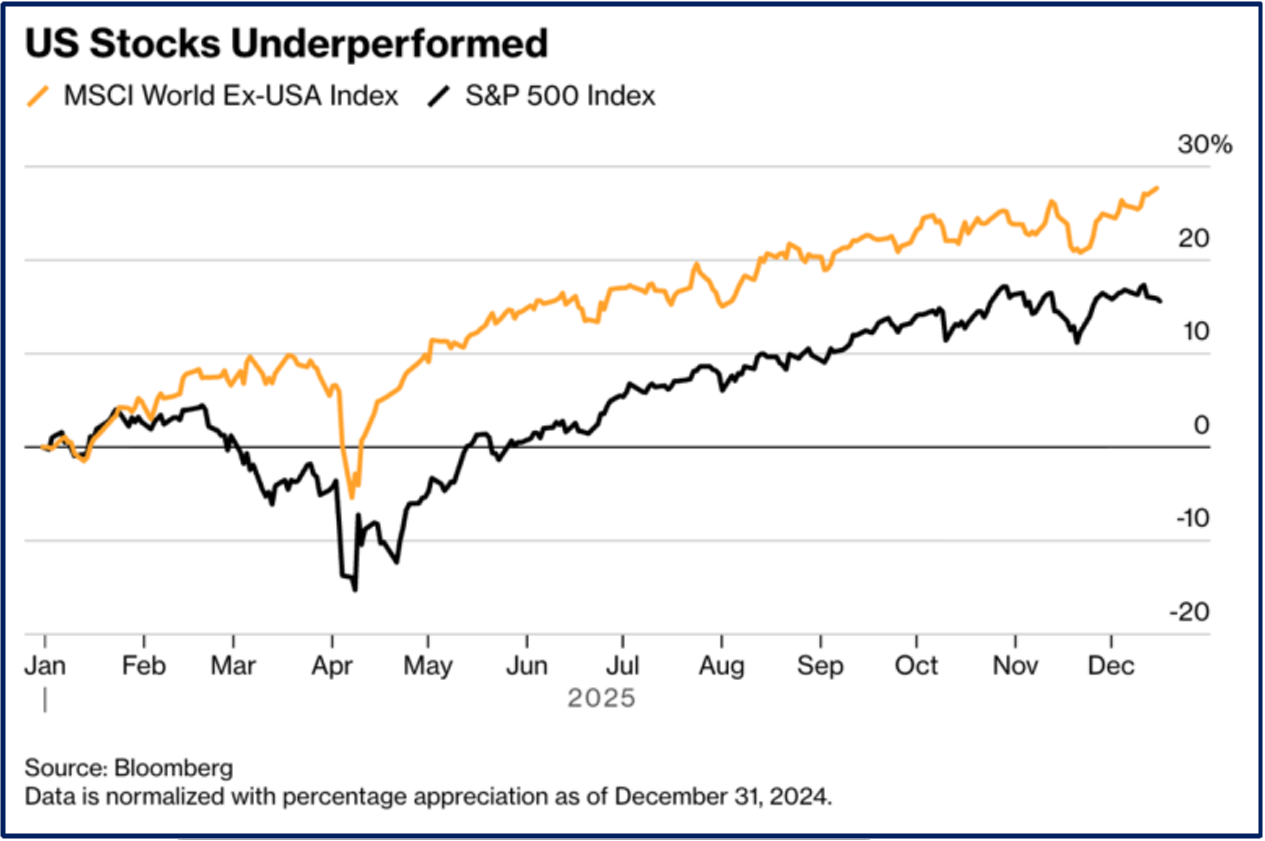

Given the S&P 500’s strong year, investors may be forgiven for not looking beyond the U.S.; however, they should. After mostly trailing U.S. stocks for more than a decade, international stocks sprang to life in 2025, with non-U.S. stocks – as measured by the MSCI ACWI ex USA Index (USD) - returning 29% for the year, outpacing the S&P 500 Index by double digits amid domestic policy uncertainty and a weakening U.S. dollar (see below graph). Yet even following that outperformance, non-U.S. equities, in aggregate, continue to trade at meaningful discounts to their U.S. counterparts, underscoring the importance of global diversification. Additionally, the MSCI EAFE Index offers a dividend yield of 3.38%, nearly three times that of the S&P 500 at 1.13%.

As noted above, one of the key drivers behind the outperformance of international equities was the sharp weakening of the U.S. dollar in 2025, fueled by trade policy uncertainty, fiscal concerns, and a narrowing yield advantage versus other developed markets. The U.S. Dollar Index (DXY), which tracks the dollar’s value against a basket of major currencies, fell nearly 10% - its steepest annual drop since 2017 - while declining even more sharply against certain individual currencies.

Economic activity in 2025 was more volatile than anticipated, as Liberation Day tariff announcements and the longest government shutdown in history heightened uncertainty among businesses and consumers. Yet despite those headwinds, the domestic economy showed surprising resilience, with third-quarter GDP growing at a strong 4.3% annualized pace - its fastest rate in two years - supported by robust household consumption and AI-related capital spending, defying earlier predictions of a slowdown or even a recession.

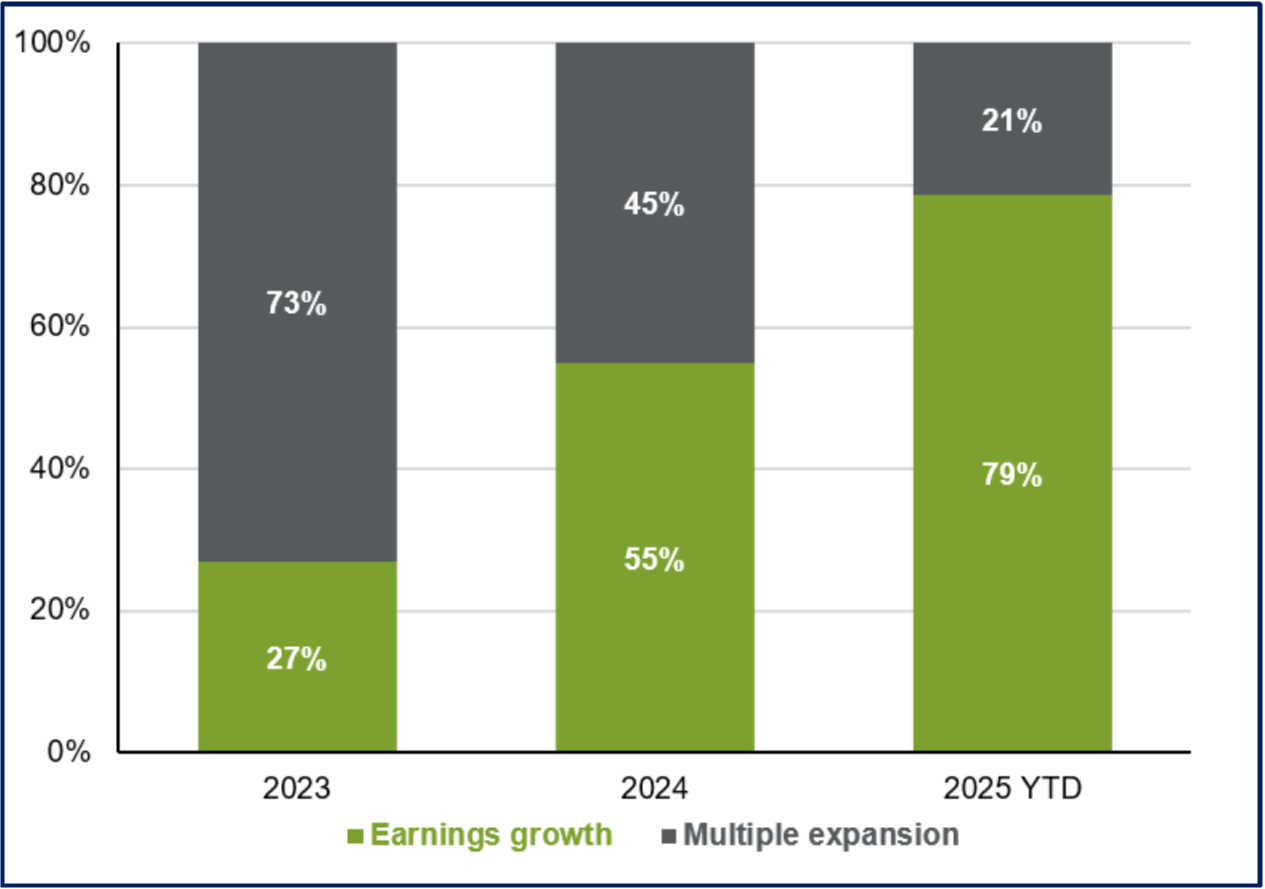

That resilience - reflected in solid GDP growth, healthy consumer spending, increased corporate investment in technology, and strong profit margins - has translated into record profits for S&P 500 companies, which were on pace to increase over 13% in 2025, with analysts expecting further acceleration in 2026. This earnings growth powered last year’s market rally, accounting for nearly 80% of the S&P 500’s return - a sharp departure from the prior two years, when rising valuations, rather than fundamentals, drove most of the gains (see the below graph by JP Morgan Asset Management).

Meanwhile, a broad-based moderation in hiring activity over recent months prompted the Fed to resume its easing cycle this fall, even as inflation remains elevated and tariff impacts have yet to be fully passed through. The unemployment rate ticked up to 4.6% in November, compared to 4.4% in September and 4.3% in August, according to the delayed November jobs report by the Bureau of Labor Statistics (BLS). Due to the government shutdown, there is no October jobs report. Still, the increase was driven less by a spike in layoffs and more by the ‘low-hire, low-fire’ environment that has characterized the U.S. labor market for months.

Fed officials have sought to navigate what they call ‘two-sided risks,’ as persistent inflation and a softening labor market complicate efforts to maintain price stability and full employment. Amid heightened labor market uncertainty, policymakers adopted a more dovish stance to support employment and initiated a series of interest rate cuts beginning in September 2025, followed by additional cuts in October and December that brought the target range for the federal funds rate to 3.50%–3.75% by year-end. It was the sixth cut to the target range since September 18, 2024.

However, policymakers have been unusually divided on the appropriate path ahead for interest rates, with some warning that further cuts could threaten the Fed’s ‘hard-won progress on inflation.’ Inflation, as measured by the core personal consumption expenditures (PCE) price index - which excludes volatile food and energy prices – remains stubbornly high at 2.8%, well above the Fed’s 2% target and unlikely to fall back to that level anytime soon. Policymakers view the PCE price index as their preferred inflation metric.

Among the world’s major central banks, the Bank of England also cut rates three times, while the European Central Bank and the Bank of Canada each opted for four cuts. The outlier was the Bank of Japan, which raised short-term borrowing costs twice to levels not seen in 30 years, taking landmark steps to unwind decades of extraordinary monetary support and near-zero interest rates.

Although central bank actions such as cuts to short-term interest rates are designed to stimulate economic activity, they do not directly translate into lower borrowing costs for consumers. A strong economy and persistent inflation can offset or dilute those effects. While 10- and 30-year Treasury yields dipped briefly after the December Fed meeting, they have since resumed an upward trend - even as markets price in one or two additional rate cuts in 2026. That divergence signals investor unease about entrenched inflation pressures and the growing supply of Treasurys tied to large and rising fiscal deficits. For the year, bonds posted solid returns, as the Bloomberg U.S. Aggregate Bond Index rose 7.3%.

Gold and silver experienced a remarkable surge in 2025, with silver jumping 140% and gold gaining 65%. This rally was fueled by dollar weakness, central bank buying, and strong ETF demand. In contrast, oil prices declined 21% in 2025, falling to their lowest levels since prices rebounded from the Covid-era crash. Bitcoin’s reputation as ‘digital gold’ was tested as the cryptocurrency fell roughly 30% from its early October high above $126,000 and closed the year down 6.4%, raising fresh doubts about its role as a safe-haven asset.

In the end, the rise in bullish sentiment reflected in BofA’s latest Bull & Bear Indicator points to a constructive close to an otherwise volatile year - one in which most asset classes ultimately generated solid returns and rewarded investors who had the discipline to stay the course. It is an important reminder for investors that although government policy plays a role, earnings growth, profit margins, and valuations are the primary drivers of long-term stock market performance.

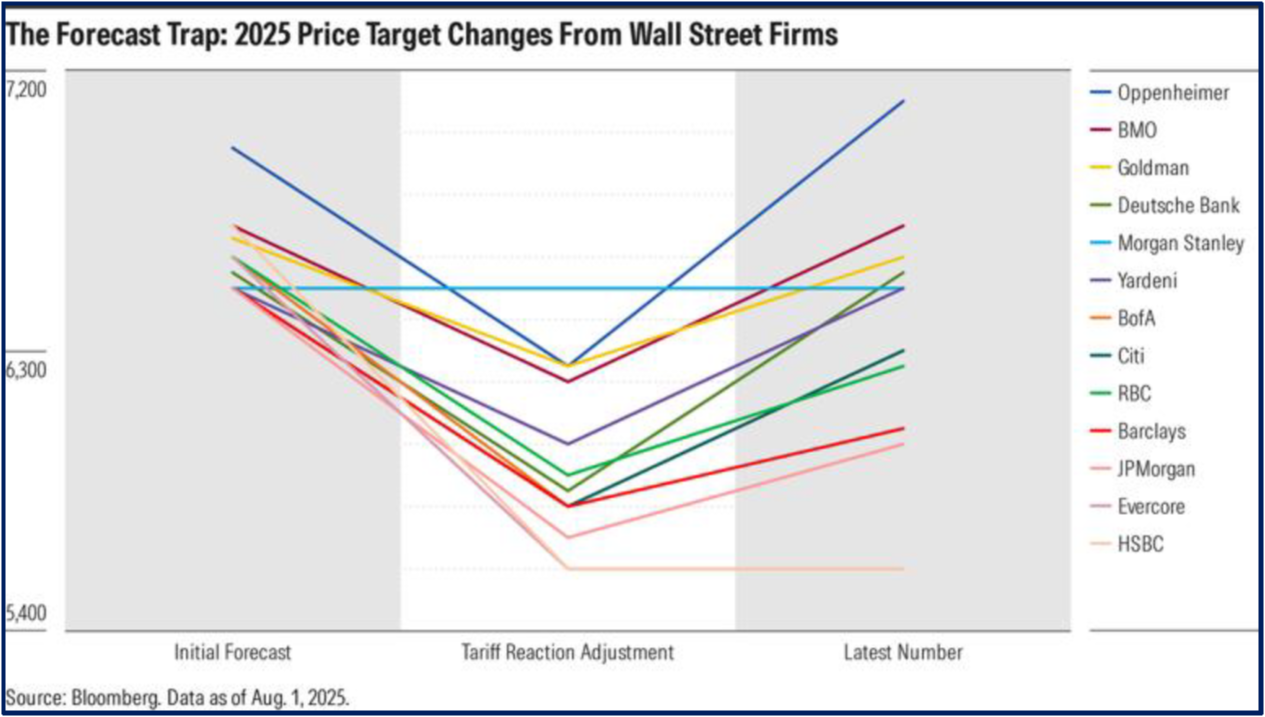

It is also a reminder that markets are unpredictable, and that attempting to forecast them, especially around the turn of the year, is a reliable way to be humbled. Morningstar’s ‘Forecast Trap 2025’ offers a textbook example (see chart below): Wall Street entered the year with high expectations for U.S. stocks, quickly lowered forecasts after the April tariff shock, and then chased the market higher again as prices recovered. The result, as Morningstar observed, is that ‘an investor blindly following those forecasts would have ended up doing exactly what we try to avoid - buying high and selling low.’

Takeaways for the New Year 2026

As investors look ahead at the start of a new year amid no shortage of forecasts and a familiar degree of uncertainty, the past year reinforces the idea that markets reward discipline, not prediction - favoring those who were prepared rather than those who claimed foresight. In that vein, here are a few key themes that can help frame portfolio decisions in the year ahead, in no particular order:

Economic growth: A modest tailwind from Fed rate cuts, fiscal stimulus from the One Big Beautiful Bill Act (OBBBA), and ongoing deregulation suggest continued U.S. economic expansion and solid GDP growth in 2026. The enactment of the OBBBA alone is expected to provide roughly $200–300 billion in fiscal stimulus this year, supporting economic activity and corporate earnings. Strong underlying fundamentals - including resilient consumer and business spending - should provide a solid foundation for markets.

Reflecting a more optimistic outlook, the Fed’s December 10, 2025, Summary of Economic Projections raised its forecast for 2026 real GDP growth to 2.3%, up from 1.8% in September. In response to U.S. tariffs and ongoing trade frictions, many countries have stepped up growth-supportive measures, including interest-rate cuts. Together, these actions are helping the global economy gain momentum as 2026 begins.

Corporate earnings: After several years of market gains driven largely by rising valuations, such as higher price-to-earnings (P/E) multiples, earnings growth has taken the lead in 2025. Corporate results have continued to exceed expectations, led by strength in the technology sector, while forward earnings expectations have remained resilient.

Bottom-up forecasts point to sustained upward momentum, underscoring robust profit growth as a key driver of equity performance. S&P 500 earnings are on pace to rise 13.2% in 2025, up from 12.1% in 2024, and are projected to accelerate further to 15.5% in 2026, according to LSEG. If companies can deliver on these expectations, the earnings backdrop could continue to support further gains in equities.

Consumer sentiment: The consumer continues to account for roughly 70% of U.S. gross domestic product (GDP), according to the U.S. Bureau of Economic Analysis. Wealthier households - responsible for more than half of total consumer spending - have been supported by investment gains and rising home values, while lower-income households are increasingly strained by higher living costs and rising student loan payments.

The labor market remains stable, and despite moderating job growth, it continues to provide a solid foundation for consumer spending. Policy tailwinds, including monetary easing and fiscal measures such as tax relief, are expected to support disposable income. Even with inflation still elevated, high asset prices have helped offset cost pressures and sustain consumer spending.

Even so, several areas bear close watching: spending by wealthier households could weaken if equity or housing markets experience a meaningful downturn.

Inflation: After rebounding to near 3% over the course of 2025, in part due to tariff pass-through, inflation is expected to moderate as the labor market cools, wage growth remains contained, and inflation expectations stay anchored. Strategists forecast PCE inflation to gradually decline to around 2.5% by the end of 2026, from 2.8% in the most recent reading, as the short-term effects of tariffs on global goods prices fade.

Despite anticipated progress, inflation remains above the Fed’s 2% target - and has not been at or below that level for roughly five years. If the Fed takes a dovish turn next year - meaning it prioritizes supporting growth through lower interest rates rather than fighting inflation - the economic expansion will likely remain intact.

Monetary policy: The risk of runaway inflation no longer appears to be the primary concern for policymakers, as signs of a softer labor market have grown in importance. As a result, monetary policy is expected to remain broadly accommodative in 2026. The U.S. Federal Reserve is likely to continue easing, with markets currently pricing policy rates just below 3% by year-end, though the pace of cuts could slow if growth strengthens or inflation proves persistent.

The appointment of the next Federal Reserve chair, expected in January, could prompt markets to price in a more dovish policy stance. Historically, periods of Fed easing outside of recessions have provided a meaningful tailwind for equities. For fixed-income investors, however, the prospect of additional rate cuts in 2026 raises the risk of lower bond yields and reduced income.

Valuations: Equities enter the new year with elevated valuations and high expectations. While fundamentals remain broadly supportive, investors may be well served by bracing for periodic bouts of volatility, given how much optimism is already reflected in stock prices.

Sustained double-digit earnings growth, bolstered by ongoing technological innovation, will be critical in justifying these valuations. The S&P 500 currently trades at more than 22 times consensus 2026 earnings per share (EPS), a valuation that leaves little margin for disappointment. Much of this valuation premium is concentrated in the AI-focused ‘Magnificent Seven,’ which now account for more than 35% of the index due to their outsized market capitalizations. This concentration highlights the importance of diversification as a risk-management tool, particularly in market-cap-weighted indexes where a narrow group of stocks drives a disproportionate share of performance.

That said, attempting to time markets based solely on valuation has historically been a poor strategy. What matters far more than any single valuation metric is the broader market context - earnings trends, credit conditions, monetary policy, corporate profitability, labor market dynamics, and investor sentiment. Viewed through that lens, the outlook for the U.S. economy and equity markets remains constructive rather than worrisome.

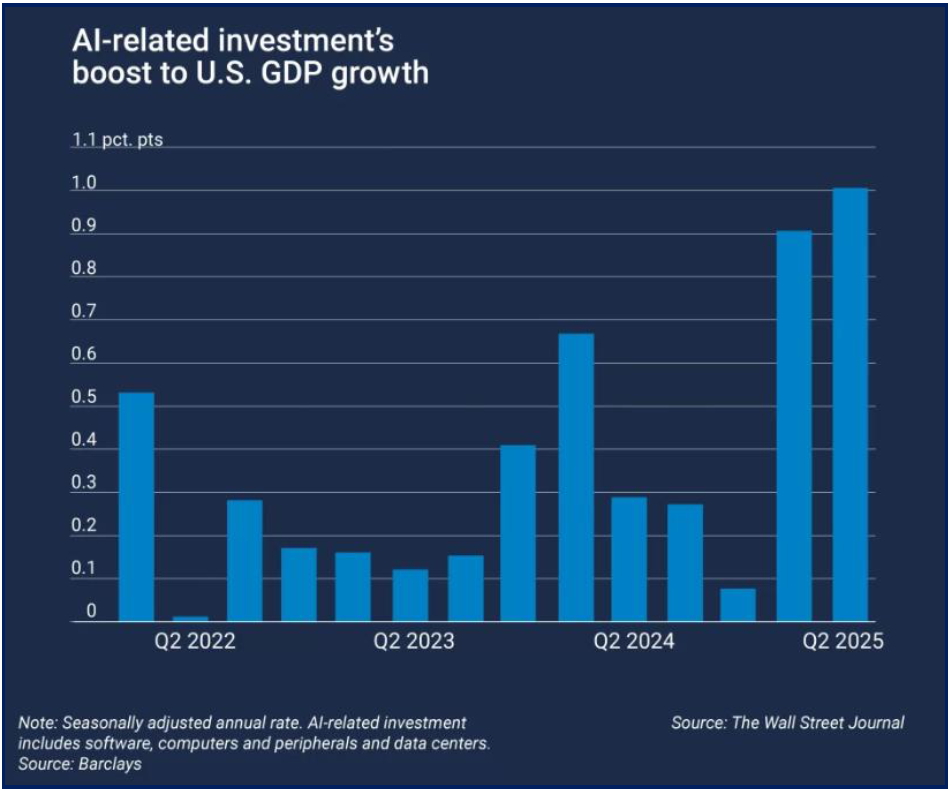

Artificial Intelligence (AI): The growth of AI may well mark the beginning of a new era, even if its full implications are not yet clear. What we can say with confidence is that it will matter - for the economy and for financial markets. The AI-driven supercycle is fueling record levels of capital spending and rapid earnings growth, with its influence spreading across regions and industries, from technology and utilities to banks, healthcare, and logistics - reshaping competitive dynamics and creating both winners and losers. AI spending has already become a pillar of US economic growth, contributing up to half of GDP growth in the first half of 2025 according to Barclays (see graph above), underscoring the scale of investment by America’s tech giants.

Still, the pace of capital deployment has pushed valuations in parts of the AI ecosystem to stretched levels, prompting legitimate questions about sustainability and the potential for froth. For investors looking ahead to 2026, the central issue is whether future cash flows will ultimately justify today’s investment surge, and whether today’s leaders will remain tomorrow’s winners. Navigating this environment will require balancing enthusiasm for innovation with disciplined analysis, selectivity, and risk management.

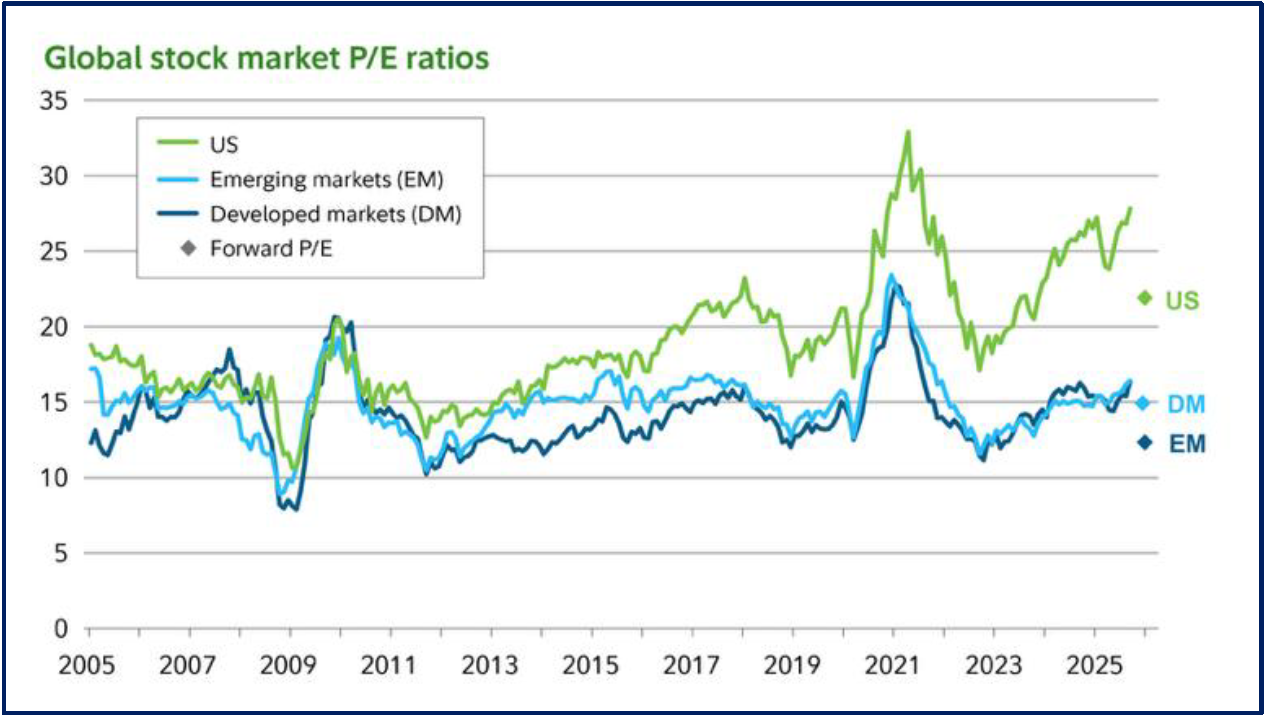

U.S. Dollar and Geographic diversification: International equities staged a strong comeback over the past year, outpacing U.S. markets by a wide margin in 2025. Even after this outperformance, non-U.S. stocks remain meaningfully cheaper - trading at roughly a 35% discount to U.S. equities based on forward price-earnings ratios (see graph above).

For investors, this combination of momentum and valuation support could prove compelling in 2026, particularly if earnings growth broadens and the U.S. dollar weakens further. A strategic allocation to international equities may enhance diversification at a time when U.S. valuations appear elevated. Importantly, non-U.S. companies make up a substantial share of global equity markets, and overlooking them risks missing a meaningful part of the global opportunity set.

Risks to watch for: Some of the biggest unknowns for investors in the coming year include AI ‘bubble’ risk, geopolitical flareups, investor reactions to rising U.S. debt levels, renewed trade policy volatility, labor market deterioration, a potential return to higher inflation, U.S. midterm elections, and, inevitably, new risks that have yet to emerge. Navigating this landscape will require maintaining perspective, adhering to a disciplined, valuation-driven approach, and embracing a healthy dose of diversification.

A Final Word

The 2026 investment landscape appears favorable for equities, supported by steady economic growth, accommodative monetary policy, stable labor markets, continued AI infrastructure investment, and corporate and individual tax cuts. These tailwinds are expected to underpin solid earnings growth and continued equity performance, although periods of volatility are likely.

Against this backdrop, we favor an actively managed approach to investing that prioritizes diversification and risk management. In our view, this is a more prudent strategy than passive exposure to a cap-weighted benchmark like the S&P 500, which remains expensive and highly concentrated in a handful of outsized technology companies.

As the New Year begins, we raise the sails and lift anchor, prepared to set out on the journey ahead alongside you. May the winds be favorable, the seas steady, and success your constant companion! Happy New Year!

JANUARY 2026