“War is the realm of uncertainty; three quarters of the factors on which action is based are wrapped in a fog of greater or lesser uncertainty.”

Carl von Clausewitz, 1780-1831; Prussian army officer and military theorist

GEOPOLITICAL TENSIONS KEEP MARKETS ON EDGE

The Prussian general and influential military theorist Carl von Clausewitz introduced the concept of the ‘fog of war’ in his seminal work ‘Vom Kriege’ (On War) in 1837 - a concept that describes the uncertainty, confusion, and limited visibility that define decision-making when clarity is most needed. It addresses the complexity of obtaining timely, reliable information in a constantly evolving environment, and the necessity of making decisive judgments with only limited information.

Though originally formulated to describe conditions on the battlefield, today’s investors operate within a similar fog, navigating an environment shaped by uncertainty, incomplete information, and the need to make disciplined decisions without the benefit of perfect clarity.

The ongoing conflict between the United States, Israel, and Iran has introduced a new layer of complexity into an already fragile global landscape. A limited military operation has rapidly escalated into a broader regional confrontation, with retaliatory strikes, disruptions to critical energy infrastructure, and rising uncertainty across global markets.

For much of the war, investors have clung to a relatively optimistic base case: that any escalation would prove short-lived, allowing markets to quickly refocus on resilient economic growth and strong corporate earnings. That narrative is now starting to weaken. Increasing signs of a broader and more sustained escalation, rather than a swift resolution, have begun to weigh on equities and other risk assets, as markets reassess the durability of the macroeconomic backdrop.

What began as a contained geopolitical shock is increasingly being reassessed by markets as a more durable source of uncertainty. With outcomes still highly uncertain, the spillover effects are extending well beyond the region, influencing energy markets, inflation expectations, central bank policy trajectories, and overall investor sentiment.

After four weeks of war, the S&P 500 traded nearly 9% below its last record high reached on January 27, while more than half of Russell 3000 stocks were down over 20% from their 52-week highs, as investors grappled with the consequences of a blockade of the Strait of Hormuz - one of the world’s most critical energy chokepoints, handling roughly 20% of global oil supply and a significant share of Liquefied Natural Gas (LNG) shipments - which sent oil prices sharply higher. For the first quarter, the Nasdaq declined 7.1% while the S&P 500 dropped 4.6%, the worst performance since the second quarter of 2022, when inflation hit a multidecade high.

Since the fighting began at the end of February, oil prices have nearly doubled from where they stood at the beginning of the year, fueling fears of inflation as companies and consumers pay more for energy products. Should the strait stay closed, the world would have to significantly reduce its oil and gas consumption - but not before prices spike to a level that forces consumers and businesses to fly, drive and spend much. less. Already, demand has begun to soften, with some countries in Asia hoarding and rationing fuel. At the same time, key Gulf producers have started to curtail output as regional storage capacity becomes increasingly constrained. Even when the strait opens, flows will take months to return to normal, including for producers that have not sustained damage in the war. A sharp move upward in the value of the U.S. dollar has compounded international worries by making the cost of purchasing oil - which is largely traded in U.S. dollars - even more expensive. This dynamic is particularly acute for import-dependent economies, whereas the United States is relatively well positioned given its limited reliance on Middle Eastern supply and minimal near-term risk of disruption.

At this stage, oil prices have yet to reach panic levels. Futures ended the month of March north of $100 a barrel for the first time since 2022, up roughly 60% since the war began, but far below 2008’s all-time high of $147.50 - a nominal peak that would be meaningfully higher in today’s dollars. European natural gas prices are up more than 70% since the start of the conflict but remain well below the record levels seen during Europe’s 2022 energy crisis.

Yet for the global economy, the shock from the Iran war has already begun. The sharp rise in oil prices risks stoking inflationary pressures while simultaneously weighing on consumer demand and broader economic growth. Such a scenario would complicate the Federal Reserve’s dual mandate of price stability and maximum employment, as the two objectives could begin to pull in opposite directions. This inherent tension reflects the core challenge of modern monetary policy and underscores the difficult trade-offs the Fed must navigate.

Over time, the central bank’s ability to adjust interest rates to blunt the effects of both inflationary pressures and labor market weakness has helped smooth the business cycle and reduce economic volatility. That flexibility has also allowed policymakers to respond when conditions deteriorate, and financial stability is at risk.

In practice, setting interest rates is an ongoing balancing act between these two objectives, requiring the Fed to constantly weigh competing economic forces. Typically, when prices are rising, policymakers raise rates to ward off further inflation. When joblessness increases, they cut rates to lower borrowing costs and spur hiring. In most cycles, these objectives pull in the same direction.

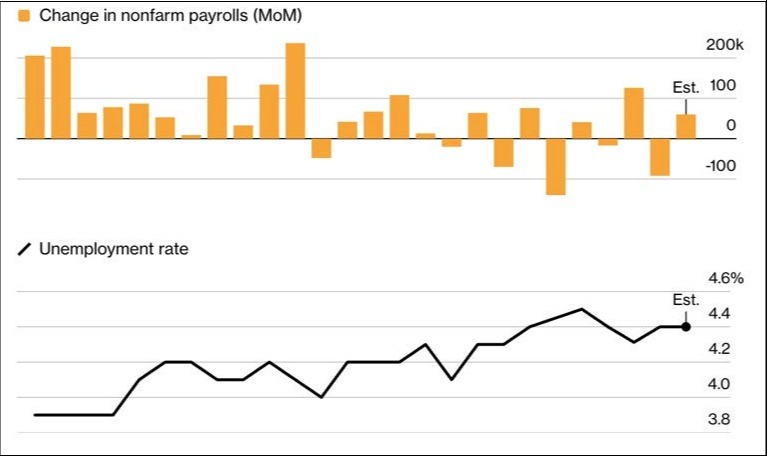

This time, however, the backdrop is markedly different. The war in Iran has sent oil prices soaring, threatening to add to global inflationary pressures. At the same time, the U.S. labor market has begun to soften, even as inflation remains elevated, placing the two objectives at odds. That pressure is increasingly evident in the data. Bloomberg Economics’ big data price tracker put the CPI for March at 3.4% year on year - a marked increase from 2.4% in February, with rising fuel prices the main culprit. Official confirmation will come with the Bureau of Labor Statistics’ March CPI release on April 10, set against the Federal Reserve’s longstanding 2% inflation target.

Meanwhile, payrolls haven’t increased in consecutive months since May of last year (see graph above), illustrating a labor market that lacks meaningful hiring momentum but also shows few signs of a concerning deterioration - what Fed Chair Powell has characterized as a ‘no hiring, no firing’ environment. While layoffs remain historically low as firms continue to hoard existing talent, new hiring has effectively stalled across several key sectors, including technology and manufacturing.

This creates a dilemma for the Fed: it can either ease policy to support labor market conditions or tighten policy to contain inflationary pressures, but it cannot do both simultaneously.

Market expectations are now reflecting this tension. According to CME Group’s FedWatch tool, the probability of a rate increase by year-end briefly surpassed the 50% threshold for the first time in late March amid inflation concerns, before reversing course toward the end of the quarter. That’s a stunning reversal from the rate-cut narrative that has dominated market thinking for the better part of two years. A one-two punch of resurgent inflation and higher interest rates would pose a far greater risk to the U.S. economy than the recent spike in oil prices alone, and could revive the specter of stagflation, the toxic combination of stagnant growth and rising prices that last haunted the domestic economy in the 1970s. Stagflation is the Fed’s worst nightmare. It forces policymakers to prioritize one side of the mandate at the expense of the other, risking failure on both fronts. At the same time, markets appear to be pricing in very little risk of recession.

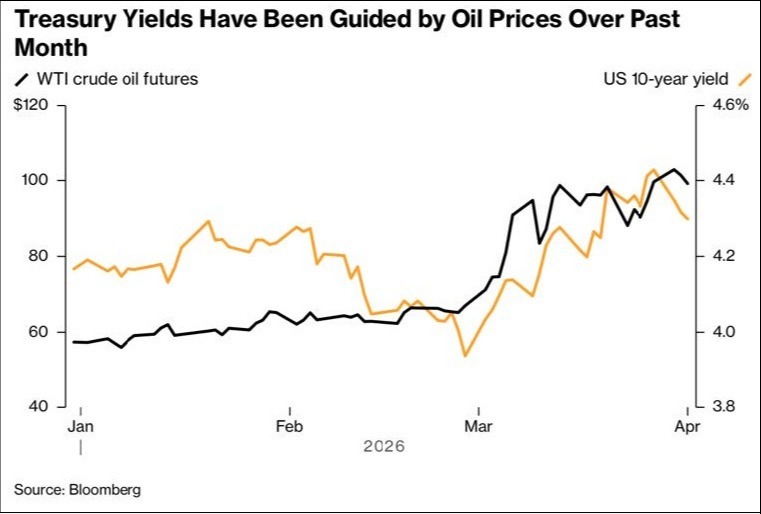

The 10-year U.S. Treasury yield, which reflects the government’s borrowing costs over a decade and underpins consumer and corporate borrowing, has tracked the war-related surge in oil prices for much of the past month because of their potential to stoke inflation and delay Fed rate cuts. The 10-year yield has surged roughly half a percentage point, from approximately 3.96% in late February to an 8-month high near 4.48% and is on course for its largest monthly gain since October 2024 (see graph above).

Not even gold was immune, as rising inflation fears effectively priced out rate cuts in 2026, leaving the metal trading around $4,650 an ounce by quarter-end, down 13% from its level prior to the war. Adding to the pressure, some central banks have become net sellers, with Turkey reportedly offloading approximately $8 billion of reserves to support its currency amid higher energy costs and increased demand for dollars.

Against that backdrop, a number of economists recently revised their forecasts for the economy downward as the war dragged on, now projecting higher inflation, slower growth, rising unemployment, and weaker consumer spending across both the U.S. and global economies in the months ahead relative to pre-conflict expectations.

The Atlanta Fed’s GDPNow estimate of real GDP growth in Q1 2026 has fallen to 1.9% (SAAR), a sharp decline from above 3.0% prior to the conflict, but still a healthy pace of expansion (see graph on this page). That weakening outlook is broadly reflected in estimates from both the St. Louis Fed (1.7%) and the New York Fed (2.1%), highlighting how the price of oil has become the dominant variable shaping U.S. growth prospects. Whether they can trigger a recession depends on how long they remain at levels that are detrimental to the economy. Markets can typically absorb short-lived oil shocks, but sustained price increases tend to filter through the economy via higher input costs, weaker real incomes, and tighter financial conditions.

If the Fed’s dual mandate wasn’t already under strain, the nomination of Kevin Warsh as the next Federal Reserve Chair - nominated by President Trump to succeed Jerome Powell, whose term ends in May - raises the stakes further, introducing questions about the Fed’s independence and potentially reshaping how the central bank navigates this stagflation-like environment. Trump has made it clear that he expects Warsh to push for substantially lower interest rates. Delivering that outcome, however, may prove easier said than done.

For his part, Warsh, who is currently a distinguished visiting fellow at Stanford University, faces a Federal Open Market Committee (FOMC) already divided over the future path of policy, with recent meetings producing closely split votes that underscore the lack of consensus within the Fed. Even so, navigating difficult decisions is nothing new for Warsh. He is a Fed veteran, having served during the critical period of 2006 to 2011 that led up to and ultimately through the global financial crisis and the central bank’s efforts to stabilize the economy. While at the Fed, he played an important role in the design and implementation of emergency lending programs aimed at stabilizing credit markets. He also played a key role in helping devise the myriad programs aimed at rescuing the economy.

Warsh’s appointment would mark a sharp philosophical shift from Powell’s pragmatic, consensus-driven approach and signal a potential lessening of the Fed’s tolerance for inflation and balance sheet expansion. He believes that productivity gains driven by AI could ease inflationary pressures, thereby enabling the Fed to lower short-term interest rates. In turn, this would shift the focus of monetary policy more toward Main Street than Wall Street. That said, an early reduction in the Fed’s benchmark interest rate could risk reigniting inflation. But before all that, he will have to be confirmed by a full Senate in which Republicans still command a majority.

Key takeaways for investors

The widening conflict involving the U.S., Israel, and Iran represents a meaningful geopolitical risk, particularly given the Strait of Hormuz’s role as a critical energy chokepoint through which roughly 20% of the world’s oil flows, along with critical shipments of LNG. In the early days of the conflict, investors largely assumed it would be short-lived, with expectations that energy flow would resume within weeks. At the time of writing, markets are still grappling with an increasingly uncertain endgame to the conflict. Questions remain around the duration of military action across the Gulf region, the implications for energy markets, and the magnitude of second-order global economic effects.

Markets have been gripped by volatility and sharp swings in the month since Operation Epic Fury began, as investors assess whether military operations will come to a quick end or escalate into a wider regional conflict. Price declines across global stock and bond markets were initially contained but intensified as concerns about a prolonged conflict pushed oil prices higher. It was a challenging quarter for equity markets, which - despite a late rally on the final day - still recorded their worst performance in nearly four years.

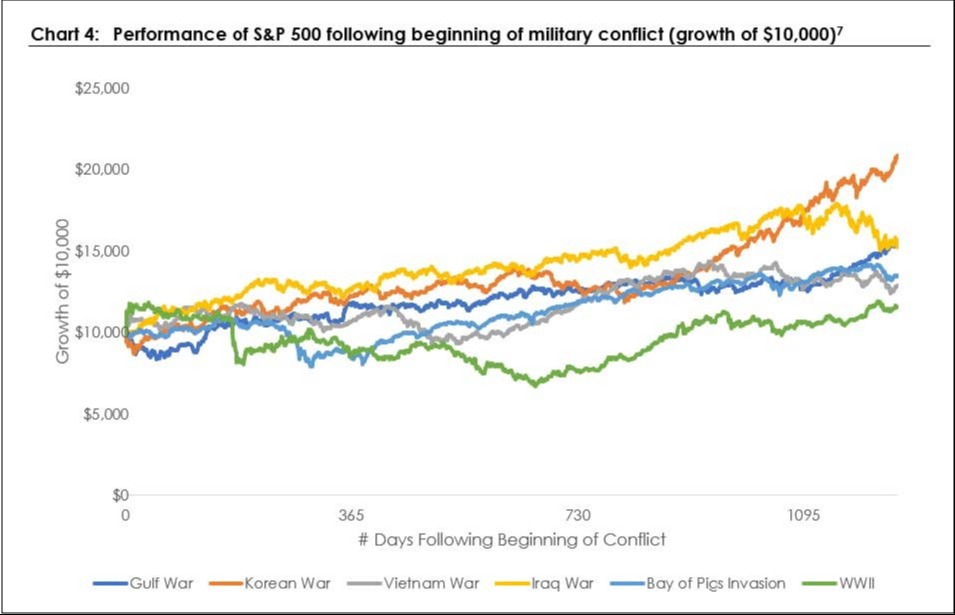

True to Clausewitz’s concept of the ‘fog of war,’ uncertainty has become the defining feature of the current environment, with neither central banks, politicians, nor oil traders having any real clarity on what comes next. While each conflict is different, the top graph on this page, courtesy Mass Mutual, tells a very important, and somewhat reassuring, story. A historical analysis of U.S. stock market performance during times when the U.S. has threatened or used military force abroad shows that the long-term market impact from geopolitical events has typically been limited. In fact, since the 1990s, the S&P 500 has been higher on average one, three, six and twelve months after geopolitical events. That resilience reflects a core reality: over time, equity markets are driven by fundamentals, which are earnings, economic growth, and interest rates. As long as those fundamentals remain supportive - and they have been, with earnings estimates rising in March - markets have consistently shown an ability to recalibrate and move forward.

Within equities, there has been rotation rather than broad-based selling, with energy and defensive sectors showing relative resilience while rate-sensitive areas have lagged. International markets have come under greater pressure, which is not surprising given that countries heavily dependent on Persian Gulf energy imports face greater exposure to this type of shock than the United States.

While military conflicts have had little long-term impact on equities, they may still contribute to bond market volatility, given their fiscal cost and the potential for longer-term pressure on public finances, which can weigh on bond prices. Bond markets are also responding to shifting inflation expectations, as higher oil prices feed through into higher yields via renewed inflation pressures.

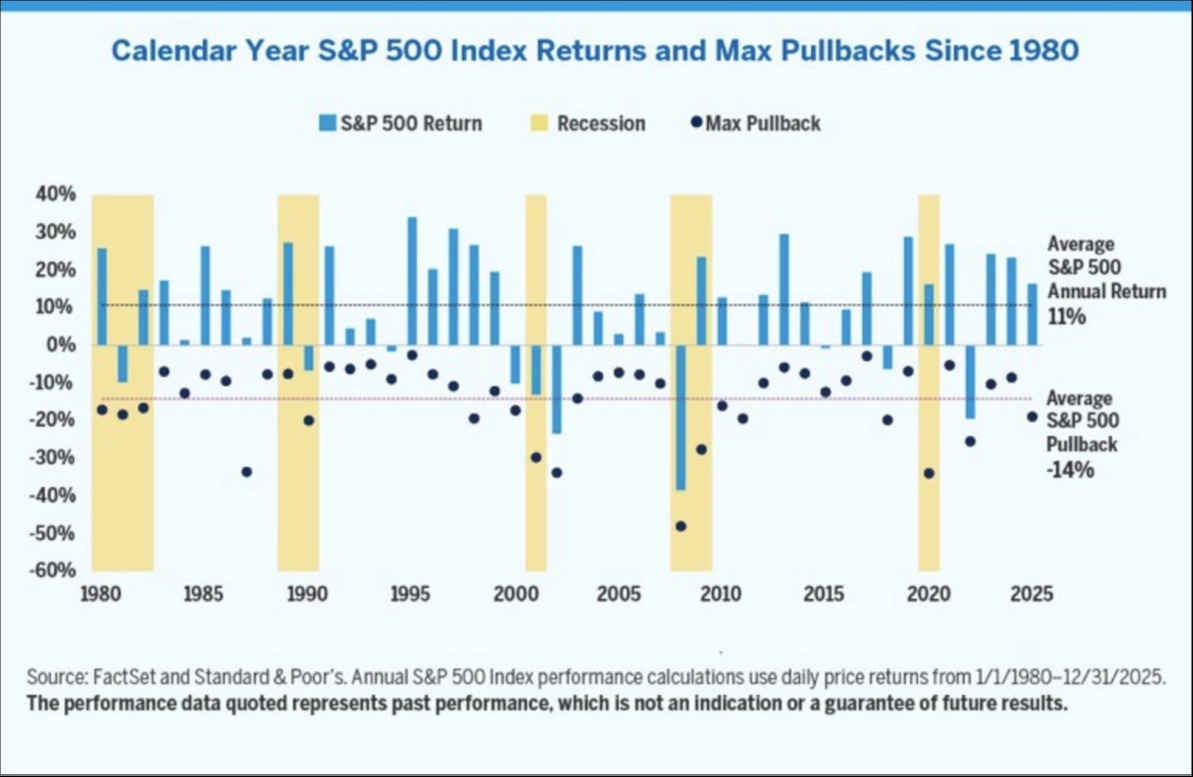

Market corrections are a normal feature of investing, and this year is unlikely to be an exception. As shown in the accompanying chart on the bottom of this page, the S&P 500 has experienced an average intra-year decline of roughly 14% since 1980, yet has ended the year positive in most instances. This underscores the importance for long-term investors to remain focused on their financial goals, maintain disciplined portfolio allocations, trust a sound process, and adhere to a well-structured investment plan, even amid short-term volatility.

At the same time, volatility cuts both ways, with periods of market stress often creating opportunity. Periods of market weakness can create attractive entry points to strengthen your investment portfolio by acquiring high-quality assets at more favorable valuations. Companies with durable business models and a consistent record of profitability are often caught up in broad selloffs, offering compelling entry points for patient, long-term investors.

Successful investing isn’t about predicting the future - it’s about preparing for a range of possible outcomes. One of the most effective ways to do that is by consulting your Telos wealth adviser, whose experience and perspective can help guide your decisions, keep you grounded, and avoid the costly mistakes that often accompany emotional investing. Our goal is to empower you to make thoughtful, informed investment decisions so your capital can work harder and more effectively for you - both today and over the long term.

APRIL 2026

GEOPOLITICAL TENSIONS KEEP MARKETS ON EDGE.pdf