Economic & Market Summary Q3 2025

____________________________________________________________________

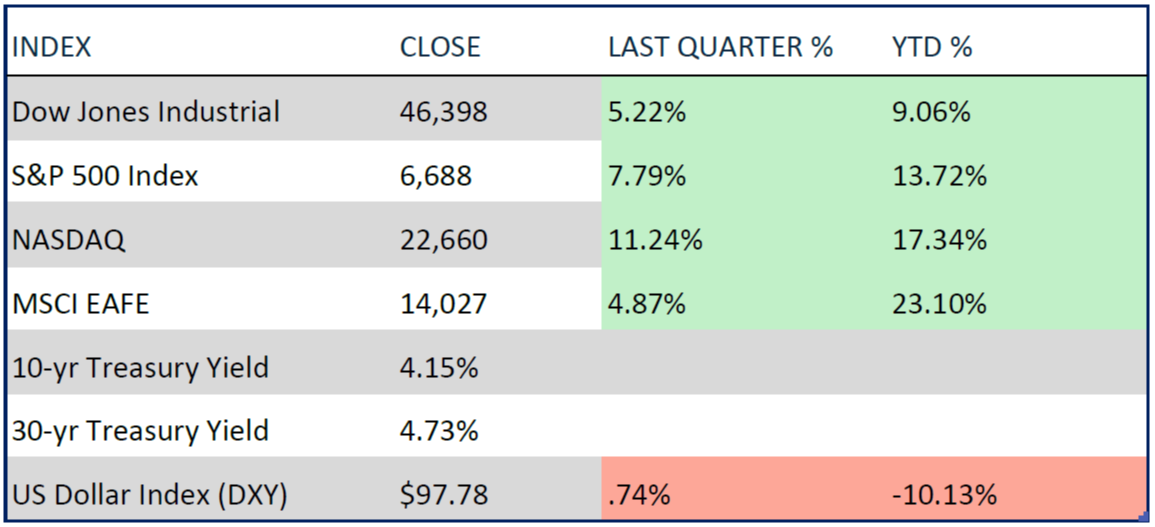

Market Summary September 30, 2025

___________________________________________________________________________________________

Stock Market

Stock Market

September is supposed to be Wall Street’s notorious villain, rattling the stock market and driving investors to panic - but this year, it eschewed the role. Interest rates are coming down; earnings growth remains robust; the job market is cooling but not cratering; tax cuts are poised to bolster corporate coffers; and the benchmark S&P 500 - up more than 13% so far this year - just finished its best September in 15 years, fueled by optimism over artificial intelligence (AI), Q2 earnings that surprised to the upside, and lower rates. The S&P 500 has posted gains for a fifth consecutive month, including a more than 7% increase in the third quarter, according to FactSet data. The Dow Jones Industrial Average and Nasdaq composite are up 9% and 17%, respectively, while the Russell 2000 index, which tracks smaller U.S. companies, recently closed at its first all-time high since 2021. Investors have a lot to feel happy about these days - and that’s before what is historically the strongest quarter of the year.

If bull markets do indeed “climb a wall of worry,” as the Wall Street idiom suggests, then there appears to be ample fuel to keep this year’s rally going, at least in the near term. On top of ongoing trade uncertainty, a weaker labor market, and geopolitical unrest, investors now have a potential government shutdown to stress over.

So far in 2025, markets have provided a vivid example of why diversification is important. As of September 30, the MSCI ACWI ex. US Index, which tracks global stock markets, has delivered roughly twice the return of the S&P 500 with lower volatility. While international stocks have soundly beaten U.S. equities so far in 2025, asset managers generally expect overseas markets to continue to outperform in the near-to-medium term, as many international stocks trade at prices that may not reflect their potential for delivering attractive returns in the future. Even after the announcement of tariffs, emerging-market (EM) stocks remain deeply discounted relative to U.S. stocks and are near historical lows. Chinese markets saw the strongest returns, climbing 20.1% for the quarter. Canadian markets outperformed the U.S. with gains of 10.4%, while Japanese markets returned 8.57%.

Meanwhile, European markets lagged, with the Morningstar Eurozone Index rising 4.15% for the quarter after second-quarter gains of more than 15.00%.

Outlook: October is traditionally a tough month for stocks, and many investors see signs of overheating - from surging speculation on meme stocks to stretched corporate valuations (see more in our newsletter). However, the fourth quarter tends to be ‘even more bullish’ in years when the S&P 500 has year-to-date gains through the first three quarters, according to Bespoke Investment Group. Since 1928, when the S&P 500 had year-to-date gains heading into the fourth quarter, it has averaged a 4.4% return during the fourth quarter, with gains 83.1% of the time, the firm said.

_______________________________________________________________________________________________________________

Bond Market & Interest Rates

Bond Market & Interest Rates

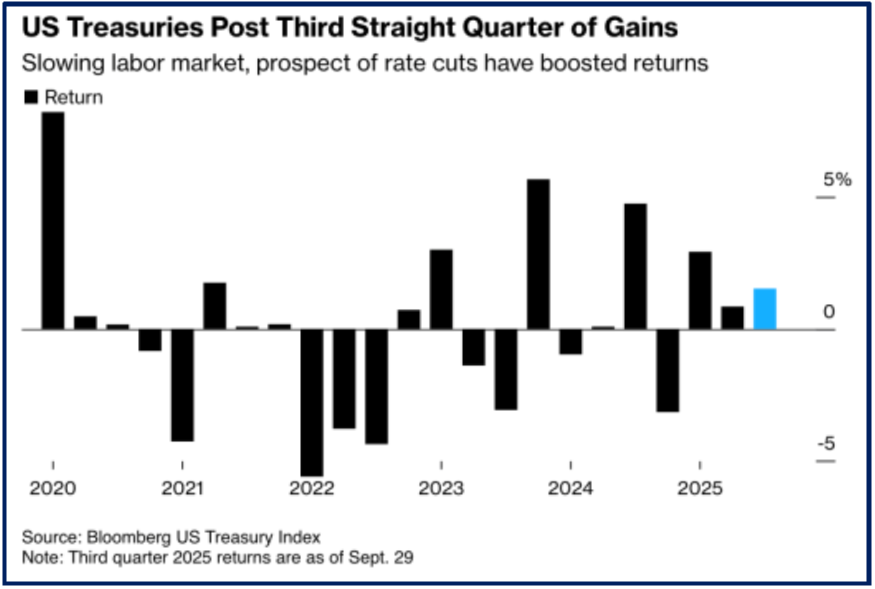

Treasuries gained for the third straight quarter, as the prospect of more interest-rate cuts has helped boost government bond prices. That has driven the 10-year Treasury yield, a key benchmark for borrowing costs for individuals and companies, down to 4.15%, below where it ended in June. The two-year yield, which stands at 3.59%, is near its lowest level over the past year. Through the first three quarters of the year, Treasuries have returned more than 5%, setting them up for the best year since 2020. Corporate bonds have also rallied, shrinking the extra return investors demand to hold companies’ bonds over risk-free Treasurys to its lowest level in decades.

The subdued job creation observed in recent labor market reports has shifted monetary policy sentiment toward a renewed focus on the employment side of the Federal Reserve’s dual mandate of ensuring price stability and promoting maximum sustainable employment. In response, the central bank implemented a 25-basis point rate cut in September, lowering the target range to 4.00%–4.25%, with updated projections showing stronger growth, higher inflation, and lower unemployment through 2026–27. It was the first rate cut of the year. While shorter-term US Treasury yields have fallen, yields on longer-dated bonds have remained elevated, thanks to the threat of higher inflation and investor concerns surrounding the federal deficit. In Wall Street lingo, that means the yield curve (a snapshot of the US Treasury market) has been steepening. For bond investors, a steeper curve provides opportunities to capture higher yields in longer-dated bonds. On the other hand, longer-dated bonds could be subject to volatility, thanks to fluid fiscal and trade policy, an uncertain economic outlook, elevated inflation, and political pressure on the Fed.

Mortgage rates edged higher over the past year. As of September 25, the average 30-year fixed rate reached 6.30%, up from 6.08% a year earlier, while the 15-year fixed rate rose to 5.49% from 5.16%.

_________________________________________________________________________________________________________________

Economic Landscape

Economic Landscape

Real GDP grew at an annual rate of 1.6% in the first half of 2025, and forecasts indicate a strong third quarter as financial conditions and positive wealth effects are supportive of economic activity. Publicly traded companies reported solid earnings and revenues in the first half of the year, and earnings guidance for the third quarter was mostly positive. Retail sales in August were solid and consumers remain resilient. The unemployment rate, wage growth and low level of layoffs are all indicative of a market around full employment, even though labor market risks appear weighted to the downside. Given the economic outlook and balance of risks, the FOMC lowered its policy rate last month by 25-basis-point as a precautionary move intended to support the labor market at full employment and against further weakening. Inflation remains nearly a full percentage point above the FOMC’s 2% target.

- GDP: GDP growth rose at an annualized rate of 3.8% from April through June, the Commerce Department said in its third and final estimate, as the import surge in the first quarter, before tariffs took effect, subsided, removing a major drag on the economy. That’s significantly higher than the 3.3% rate reported in the second estimate, and a dramatic upgrade of its initial estimate of 3%. Personal consumption expenditures rose at an annualized pace of 2.5% in the second quarter, according to the third estimate, up sharply from the second estimate’s 1.6%. Conversely, imports declined at an annual rate of 29 percent in the second quarter, which boosted GDP growth by more than five percentage points (imports are a subtraction in the calculation of GDP). The Federal Reserve Bank of Atlanta estimates that GDP continued to power through at a robust pace in the third quarter, forecasting third-quarter GDP to register at a strong 3.9% rate. Forecasters expect U.S. GDP growth of 1.9% in 2025 and 1.8% in 2026 - both up slightly from their previous forecasts.

- Inflation: The Federal Reserve’s preferred inflation gauge reached its highest level in six months as it edged further away from the 2% target. The Core Personal Consumption Expenditures (PCE) Price Index, which excludes volatile food and energy costs, rose 2.9% year-over-year in August, a slight pickup from July. Meanwhile, the headline index jumped to its highest level since April 2024, rising 2.7%, as expected. Consumer prices rose across the board, with both goods and services ticking higher. The Fed targets inflation at 2%, a level where it has not been since early 2021.

- Consumer spending: Consumer spending, which accounts for more than two-thirds of economic activity grew by 0.6% in August, the Bureau of Economic Analysis reported Friday. That’s higher than July’s 0.4% pace. The increase, fueled by rising compensation, shows households are still willing to spend even as inflation remains elevated.

- Unemployment: Labor Department revisions earlier this month showed that the economy created 911,000 fewer jobs than originally reported in the year that ended in March. That meant that employers added an average of fewer than 71,000 new jobs a month over that period, not the 147,000 first reported. Since March, job creation has slowed even more — to an average of 53,000 a month. On Oct. 3, the Labor Department is expected to report that employers added just 43,000 jobs in September, though unemployment likely stayed at a low 4.3%, according to forecasters surveyed by the data firm FactSet.

__________________________________________________________________________________________________________

Currency & Commodity Markets

Currency & Commodity Markets

At the beginning of the year, both the dollar and the stock market were in positions of strength, with the S&P 500 near record highs and the dollar at its strongest since 2022, as measured by the U.S. Dollar Index (DXY), which measures the intrinsic value of the U.S. dollar against a basket of major developed-market currencies. Both stocks and the dollar stumbled at the start of the year, but the stock market has since fully recovered from its April low. The U.S. dollar, however, remains down roughly 10% year-to-date - the most at this stage of a year since 1989 - even though the U.S. economy has demonstrated resilience. The currency gained 1% in the third quarter, largely thanks to a weaker Yen. Several factors have weighed on the dollar’s value, most notably: economic uncertainty stemming from the trade policies implemented by U.S. President Donald Trump, and the downgrade of U.S. sovereign credit ratings by the three major rating agencies—S&P Ratings, Fitch Ratings, and Moody’s Credit Rating. A recent Bank of America survey shows global fund managers at their lowest USD allocation since 2005.

The U.S. currency depreciation could have significant impacts for consumers, businesses, investors and ultimately for the overall economy: It would be more expensive for Americans to travel abroad. U.S. assets could be less compelling for foreign investors. Import prices could rise, putting pressure on inflation. On the positive side, however, the weaker dollar could be a boost for American exporters. At some point the tide may well turn back, but for now the combination of international trade tensions, large federal deficits, and European strength continue to put downward pressure on the dollar.

Gold, often viewed as an inflation hedge and a haven for nervous investors, are on pace to notch their best first three-quarters of a year since 1979, soaring more than 45% this year. Silver is up 61%, nears its own record. The deadlock in Washington is the latest turmoil boosting gold’s appeal as a safe haven, along with concerns about geopolitical tensions and the economic impact of the tariffs.

___________________________________________________________________________________________________________

Political & Geopolitical Developments

Political & Geopolitical Developments

Tariffs and trade:

- Trade deals with Japan and the European Union have reduced the uncertainty that exporters and importers face, but at the cost of new tariffs that will hit importers and consumers. The effective tariff rate on imports is now around 15% across all goods. Higher rates are being imposed on common goods imports, such as home furnishings, toys, sports equipment and the like, but have not had a large impact on the Consumer Price Index yet. Price increases on motor vehicles will likely be coming later in the year as inventories of pre-tariff imported vehicles run low. However, tariffs will likely not cause a broader recession in the economy.

Government shutdown:

- The federal government is shutdown, with Congress unable to reach a funding agreement before the start of the new fiscal year, 1 October. As both chambers narrowly divided and deeply polarized, the pressure builds with Washington’s budget battles. With the full government shutdown, hundreds of thousands of federal workers are furloughed and required to work without pay. Operations deemed essential - such as social security, military duties, immigration enforcement, and air traffic control - continue, but other services may be disrupted or delayed as the days drag on. Government shutdowns are typically a political headache rather than an economic one. The broader equity market has a habit of ignoring budget fights: The S&P 500 Index has barely moved on average across the last 20 shutdowns, according to data compiled by Truist. While the broader economy may not feel the effects immediately, analysts warn the prolonged shutdown could slow growth, disrupt markets, and erode public trust.

October 2025

Economic & Market Summary Q3 2025 PDF