“The pessimist sees difficulty in every opportunity. The optimist sees opportunity in every difficulty.”

Sir Winston Churchill, 1874 - 1965; former Prime Minister of the United Kingdom from 1940 to 1945

DEBT, DEFICITS, AND THE IMPLICATIONS FOR INVESTORS

In 1989, disturbed by the country's escalating debt, Seymour Durst, a prominent New York real estate developer, installed an odd-looking digital billboard on the corner of Sixth Avenue and 42nd Street in Manhattan. Unlike the dazzling ads of nearby Times Square, this one didn't promote electronics or clothing. Instead, it displayed one number - and that number kept climbing. Durst called it the 'National Debt Clock,' a real-time display of all outstanding debt owed by the federal government - the U.S. national debt. It was his way of highlighting the rising government debt and encouraging people to think about fiscal responsibility. He is famously quoted as saying, "If it bothers people, then it's working."

At the time, the national debt stood at around $2.7 trillion, representing about 50% of the gross domestic product (GDP). Since then, the clock has moved locations, added digits (when the debt surpassed $10 trillion in 2008), and expanded its display to include per-family and per-citizen debt figures.

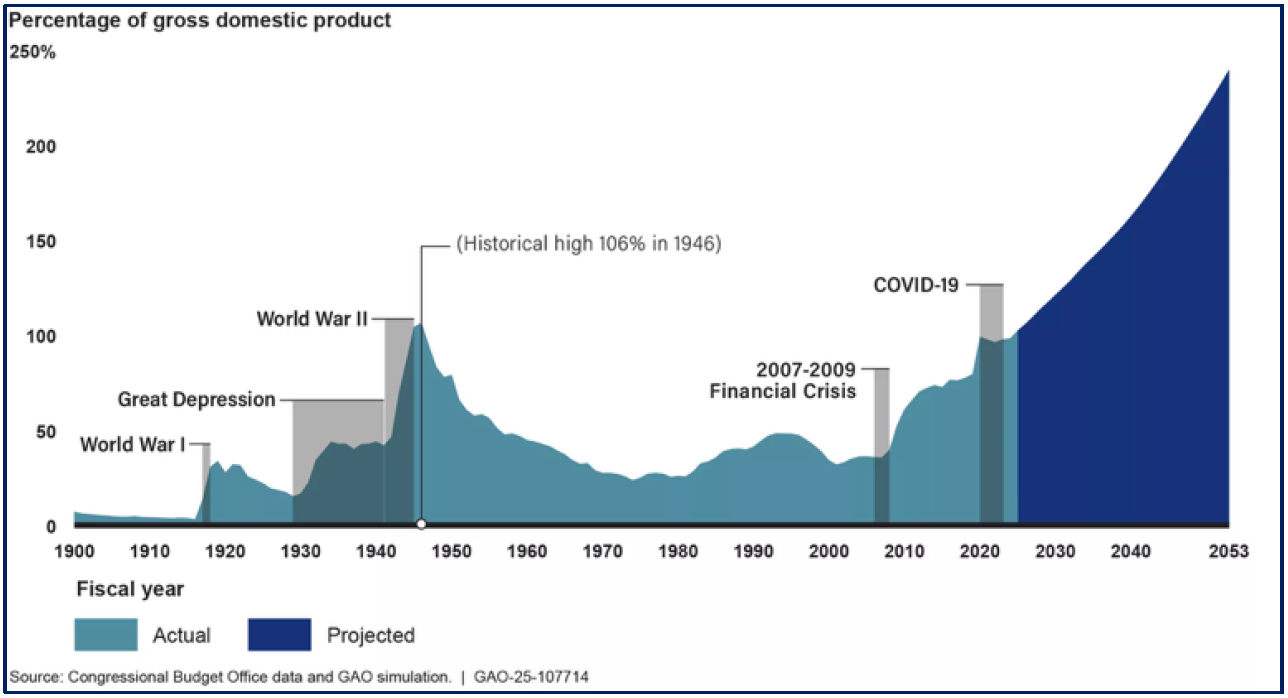

Fast forward to today: the U.S. national debt now surpasses $37 trillion - a six-fold increase in the 21st century alone and far outstripping last year's GDP of $29.2 trillion (see graph below). A high debt-to-GDP ratio signals that a country owes more than it produces in a given year. The combination of surging debt and rising interest rates has intensified worries among economists, credit agencies, and investors over the sustainability of U.S. public debt - and the potential risks it poses to financial stability. Additionally, the currently elevated debt-to-GDP ratio raises concerns that the debt situation could deteriorate further if the economy weakens, potentially necessitating additional fiscal stimulus.

While markets have so far absorbed large deficits - the imbalance between the money a government spends and what it collects from taxes in a given fiscal year - without immediate consequence, the long-term risks are mounting. These deficits have historically widened significantly in the aftermath of recessions and cries, with the government relying on the issuance of U.S. Treasury bonds to finance the shortfall. During the last full fiscal year, that deficit, totaled $1.8 trillion. The national debt represents the accumulated total of all deficits over the years by the government, which currently exceeds $37 trillion, or over $108,000 for every single American. At the current pace, the debt could reach $40 trillion this year, doubling in just eight years since 2017. To put this in perspective: it took 220 years for the U.S. to accumulate its first $11 trillion in debt!

The combination of rising debt and higher interest rates has more than doubled the average cost of the Treasury's overall debt from 1.55% in early 2022, to 3.35% at the end of March. Rising interest costs are now one of the fastest growing components of federal spending. According to Federal Reserve Bank of St. Louis data, the U.S. spent $1.1 trillion in interest to service its debt in FY 2024, an amount that surpasses spending on both, national defense and Medicare. Increases in these payments divert capital resources from critical areas like infrastructure, education, and healthcare, and can hinder long-term economic growth. This 'crowding out' effect also discourages private investment due to higher borrowing costs.

The U.S. fiscal trajectory garnered significant attention back in August 2011, when Standard & Poor's (S&P) did what no one thought possible - it became the first major credit rating agency to strip the United States of its prized AAA rating, downgrading it to AA+ and sounding the alarm on America's growing debt burden. Citing 'political brinkmanship' in Washington as a factor in the downgrade, S&P warned at that time that U.S. debt as a percentage of GDP was on an unsustainable trajectory, and that future debt service costs could crowd out spending on essential programs or trigger economic strain.

More than a decade later, in August 2023, the U.S. faced another blow to its credit standing when Fitch Ratings also downgraded the country's long-term debt from AAA to AA+. Their rationale echoed many of the same warnings from 2011: rising debt levels, deteriorating governance, and repeated brinkmanship over the debt ceiling. After years of warnings and outlook revisions, Moody's finally joined its peers in May this year by downgrading the U.S. sovereign credit rating from Aaa to Aa1, becoming the last of the legacy rating firms to take that step.

These rating downgrades reflected not only ballooning deficits and burgeoning debt, but Washington's repeated willingness to weaponize the debt ceiling, which is the total amount of money that the U.S. government is authorized to borrow to meet its existing legal obligations. After being suspended in 2023 - allowing the federal government to borrow as needed - the limit was restored on January 2, 2025, and set to the outstanding debt level of $36.1 trillion at that date. Since then, the Treasury Department has been using accounting maneuvers called 'extraordinary measures' to pay its bills and extend the date when it will run out of money. Extraordinary measures are authorized by law to allow the Treasury to generate additional cash on hand to fund obligations when borrowing is at or near the debt limit.

Treasury Secretary Scott Bessent warned that the federal government will hit its statutory debt ceiling - the so-called 'X Date' when the country runs short of money- as early as August, unless Congress enacts legislation to avoid a Treasury default by either raising or suspending it. He subsequently urged lawmakers "to act promptly to protect the full faith and credit of the United States."

Typically, the debt ceiling is raised without much fanfare, and a default on U.S. debt has never occurred. Yet lawmakers frequently wait until the last minute to raise or suspend the debt ceiling. Such irresponsible fiscal brinkmanship has previously led to U.S. credit rating downgrades and remains a recurring source of anxiety and volatility in financial markets. For instance, observations based on prior cycles show that Treasurys that matured within the 'X Date' window declined in price (yields increased) as investors avoided ownership of those issues.

While we expect an agreement before the default date is breached, the process of reaching a deal could be drawn out and contentious as it has often been in the past. Failure to raise or suspend the debt ceiling in a timely manner could trigger market volatility both domestically and internationally, elevate borrowing costs, and weigh on economic growth.

The more serious concern isn't the next deadline, however - it's the long-term fiscal trajectory that most economists agree is unsustainable without significant policy change. According to the nonpartisan Congressional Budget Office (CBO), the U.S. faces mounting deficits and surging interest expenses that will continually exceed potential GDP growth - a dynamic typically seen only during economic crisis - with public debt projected to climb from about 120% of GDP today to 166% by 2054 under current law. As currently proposed, the administration's 'One, Big, Beautiful Bill' could add several trillion dollars to the national debt over the coming decade, further exacerbating the country's already unsustainable fiscal trajectory. What is particularly concerning about the current fiscal landscape is the persistence of elevated federal deficits despite a relatively strong economy, which calls into question the government's ability to respond to future economic shocks without further undermining long-term debt sustainability.

In their popular 2011 book 'This Time Is Different: Eight Centuries of Financial Folly,' Carmen Reinhart and Kenneth Rogoff (both at Harvard) argued that rising levels of government debt are associated with much weaker rates of economic growth. Their research suggests that once debt reaches more than about 90% of GDP, the risks of a large negative impact on long term growth become highly significant. Over the entire two-century sample (from 1790 to 2009), average growth plunged from more than 3% a year to just 1.7% once debt rose above that critical level. The authors warn that the costs of even moderately slower growth can quickly add up, since the average debt overhang lasts more than 20 years.

In recent years, debt apologists - individuals who downplay the potential negative consequences of national debt - have pointed to Japan, whose debt-to-GDP ratio is nearly double that of the U.S., as proof that a wealthy country can spend freely and incur large indebtedness without consequences. That view may be comforting - but it's dangerously misguided and ignores economic history. After its asset bubble burst in the early 1990s, Japan suffered from a prolonged period of economic stagnation, deflation and policy paralysis, a phenomenon dubbed 'Japan's Lost Decade.' Meanwhile, the stock market, as measured by the Nikkei 225, took almost 34 years to climb back to its 1989 peak- a sobering reminder that the absence of an immediate crisis doesn't mean all is well.

While the U.S. differs from Japan in many respects, the comparison still raises a fundamental question: Can a country sustain large and growing debt burdens indefinitely without eventually facing economic or market repercussions? History and economic theory suggest the answer is no. The question is, how concerned should investors be?

TAKEAWAYS FOR INVESTORS

Government policymakers and those outside of government have warned of the danger and potential negative consequences of the mounting debt for nearly half a century. Up until now, the surging national debt has yet to notably detract from economic growth or capital market performance, and it may take years, perhaps even decades, before there's meaningful pressure to curb government borrowing. Regardless of short-term market calm, the U.S. remains on a fiscally unsustainable path, and the growing national debt will eventually affect financial markets. It's hard to know when that tipping point will be, but there's a strong likelihood that a market event - not politicians or voters - will drive the eventual reckoning, with rising bond yields, falling stock prices, or a weakening dollar serving as the catalyst for change. For instance, during the 1990s, bond vigilantes - investors who protest against expansionary fiscal and/or monetary policy by aggressively selling bonds - revolted against the Clinton administration's large government spending and drove the 10-year yield from 5.2% in October 1993 to 8.0% in November 1994. In response, policymakers were forced to enact deficit reduction measures. A clear grasp of the U.S. national debt and its far-reaching consequences is critical for prudent investment decision making and for positioning portfolios to successfully navigate potential challenges ahead.

To be clear, we are not questioning the U.S. government's ability to repay its debt, as the probability of a U.S. default on its debt is virtually zero. Even after the downgrade, Moody's itself acknowledged that U.S. creditworthiness rests on 'exceptional credit strengths' such as the size, resilience and dynamism of its economy, monetary flexibility, and the government's unblemished record of honoring debt through every crisis. Nevertheless, the concerns raised by rating agencies underscore genuine fiscal vulnerabilities that must be addressed over time to maintain that credibility. As economist Herbert Stein told Congress at a national debt hearing in 1986, "if something cannot go on forever, it will stop."

No asset class generates more investor concern when it comes to the debt debate than bonds. As a government takes on more debt, creditors may demand higher interest rates to compensate for the risk of lending to a heavily indebted country. As a result, the need to finance annual deficits exceeding $2 trillion, combined with the Federal Reserve's ongoing reduction of its Treasury holdings, is likely to exert upward pressure on interest rates in the years ahead. That means higher borrowing costs and larger interest payments, which could further exacerbate fiscal stress and deepen strain on an already stretched federal budget. Potentially compounding the problem is the risk that broad or high U.S. tariffs could reduce foreign demand for Treasurys, which may further amplify pressure on interest rates. Overseas investors currently own about one-third of U.S. Treasurys, underscoring the importance of global confidence in America's fiscal outlook.

The Moody's downgrade gave investors a preview of how sensitive markets have become to fiscal concerns. Treasury yields jumped in its aftermath, with long-dated bonds rising above levels seen during April's tariff turbulence - underscoring that federal spending and debt levels are increasingly in focus for markets.

Rising interest rates increase the cost of servicing government debt, but their impact reaches well beyond the public sector. They tighten financial conditions across the economy - raising mortgage rates, increasing the cost of credit, and limiting access to capital - making it more expensive for households and businesses to borrow, invest, create jobs, and drive innovation and growth. Over time, this dynamic can dampen long-term economic growth and suppress wage gains. Multiple studies have shown a statistically significant negative correlation between elevated federal debt levels and economic growth, particularly when debt crowds out productive investment or limits fiscal flexibility.

Jitters in the bond market can also easily spill over into other asset classes, including equities and currencies. As interest rates rise, stocks may lose their relative appeal compared to risk-free returns, especially if earnings expectations are revised lower. Meanwhile, the U.S. dollar has already come under pressure this year, falling over 10% against a basket of currencies to its lowest level in three years - a rare and steep decline - as investors grow increasingly uneasy about America's deteriorating fiscal outlook.

The path forward

Recognizing the risks of excessive debt - and understanding the policy tools available - is a critical first step for lawmakers aiming to restore the U.S. to a sustainable fiscal trajectory. As in the old adage, 'When you're in a hole, the first step is to stop digging.' Reducing the U.S. national debt in any meaningful way will be a complex and politically fraught endeavor, made even more daunting by the sheer magnitude of the debt and the contentious nature of the policy changes needed.

Experts say there are three potential paths ahead:

- Austerity. This would likely involve a combination of tax increases and spending cuts, though such measures are often difficult to implement and carry significant social and economic costs.

- Inflation. This involves allowing or actively encouraging a higher rate of inflation. Inflation erodes the real value of existing debt, particularly fixed-rate debt, because the government repays creditors with dollars that are worth less in real terms. A budget model constructed by the University of Pennsylvania Wharton School projected that permanently increasing the Fed's current 2% annual inflation target to 3% would reduce the inflation-adjusted value of the federal debt by 7% by 2051, without having to lower Social Security benefits. While inflation might appear to provide temporary relief, it is not a sustainable solution and would likely lead to a decline in living standards and destabilize the economy.

- Economic Growth - our preferred approach. Sustained economic growth can help improve the debt-to-GDP ratio by increasing tax revenues without raising rates and reducing the relative burden of existing debt. While growth alone may not solve the debt problem, it can ease fiscal pressures and support a more balanced long term solution. The good news is that even just small increases in economic growth can dramatically improve the federal government's debt-to-GDP levels over time. The question is how to achieve that economic growth. Emerging technologies such as artificial intelligence (Al) could drive productivity gains and stronger economic growth, partially mitigating the long-term impact of rising public debt. Although it is still too early to quantify exactly how strong Al's economic impact may be, technological breakthroughs have been the single most important factor in driving growth for over a century. Still, there is no guarantee that productivity gains will be sufficient to address the fiscal challenges facing the U.S.

Addressing today's elevated debt burden will necessitate politically difficult decisions and a sustained focus on fiscal prudence. A durable fix will almost certainly require a mix of spending discipline, tax reform, and sustained economic growth. According to the CBO, addressing high and rising debt sooner rather than later means that smaller policy changes would be required to achieve long-term objectives. The unfortunate reality is that there appears to be little political resolve to address the deficit. In the absence of external pressure, neither party seems inclined to take meaningful action - unless a crisis leaves them no choice. As Winston Churchill once famously observed, "You can always count on Americans to do the right thing - after they've tried everything else." Unfortunately, the window for our leaders to exhaust all other options before embracing the necessary course of action is closing swiftly.

Investment implications

The soaring national debt significantly impacts financial markets, but particularly the fixed income sector. Our focus on quality shapes how we manage fiscal risk within portfolios. Well-capitalized companies are typically better positioned to withstand rising rates, and investment-grade bonds provide a more stable foundation amid concerns over government debt and market dislocation. For now, U.S. Treasury securities and other high quality fixed income investments should continue to play an important role in a broadly-diversified portfolio - despite growing concerns about the nation's fiscal trajectory.

If worries about the fiscal outlook intensify, we are prepared to adjust our portfolio positioning accordingly. Potential strategies include increasing allocations to short-term fixed income, high-quality corporate bonds, highly rated sovereign bonds from other developed economies, and Treasury inflation-protected securities (known as TlPS) to combat inflation. Diversifying multi-asset portfolios into non-U.S. dollar-denominated securities, real assets, precious metals, and select foreign currencies may offer potential hedges against fiscal instability and a weakening dollar.

Given that debt is a long-term issue, whereas equity markets tend to prioritize corporate earnings trends and economic growth momentum, elevated debt levels may not constitute an immediate concern for the stock market. Active risk management is essential to construct and maintain resilient portfolios - especially if stressed market scenarios ultimately materialize. Telos will closely monitor the government's increasing debt burden and policies that influence long-run sustainability for signs of change in the broader investment landscape.

Although the long-term ramifications of escalating U.S. debt are significant, it does not currently constitute an imminent threat to market stability. It is worth noting that past projections of fiscal crisis have often proved overstated or slow to unfold. However, turning a blind eye to the potentially dangerous consequences reminds us of a famous quote attributed to American writer and philosopher Ayn Rand: "You can ignore reality, but you cannot ignore the consequences of ignoring reality. " There is still time to address the nation's fiscal challenges - but the clock is ticking.

JULY 2025